Impermanent Loss Calculator

This calculator estimates the impermanent loss when you provide liquidity. Simply enter the weightage of the assets and the percentage change expected to estimate impermanent loss percentage. Note that this calculator does not include any trading fees earned, which may help cushion impermanent losses.

%

%

%

%

APY calculator

This calculator breaks down the annual percentage yield (APY) across different timeframes for a given principal (in $) and APY percentage to help estimate earnings.

USD

%

| Period | % Returns | Returns |

|---|---|---|

| Minutely | ||

| Hourly | ||

| Daily | ||

| Monthly | ||

| Yearly | ||

FAQ on Impermanent Loss and APY

What is APY in crypto?

APY, short for annual percentage yield, measures the rate of return when users deposit their funds into different lending and yield farming protocols. APY includes the effects of compounding interest, which can transform low daily or hourly returns into massive amounts over time. Since APY reflects the return on investment over a year, you should only expect to receive the advertised rates if your funds are deposited over that time horizon. Returns may also vary at any moment due to a multitude of factors such as token price and additional token incentives.

How is APY calculated in crypto?

In crypto, APY is often calculated differently depending on how often the yield is disbursed. For example, rebase tokens such as Olympus, Wonderland TIME, and KlimaDAO [OLD] allow depositors to earn rewards every epoch, usually every 8 hours. This means that your deposited tokens will effectively compound 3 times per day, resulting in a much higher APY than if your tokens were only compounded daily.

With that being said, the APY can also fluctuate based on the token price and the total amount of deposits. Some protocols usually provide returns in the form of other tokens, where users need to manually claim, sell the tokens and compound them to their initial deposit. The APY shown will then be the yield that depositors can expect to receive if they manually compound on a daily or weekly basis.

The general rule of thumb is that the higher the number of compounding periods, the higher the APY. Sometimes, a protocol may display the APR, or annual percentage rate, instead of APY. The critical difference is that it can be regarded as simple interest, where the effects of compounding are not included. Both protocols could have the same APR, but the APY can vary wildly based on how often new tokens are continuously added to your initial deposit.

With that being said, the APY can also fluctuate based on the token price and the total amount of deposits. Some protocols usually provide returns in the form of other tokens, where users need to manually claim, sell the tokens and compound them to their initial deposit. The APY shown will then be the yield that depositors can expect to receive if they manually compound on a daily or weekly basis.

The general rule of thumb is that the higher the number of compounding periods, the higher the APY. Sometimes, a protocol may display the APR, or annual percentage rate, instead of APY. The critical difference is that it can be regarded as simple interest, where the effects of compounding are not included. Both protocols could have the same APR, but the APY can vary wildly based on how often new tokens are continuously added to your initial deposit.

What is the difference between APR and APY?

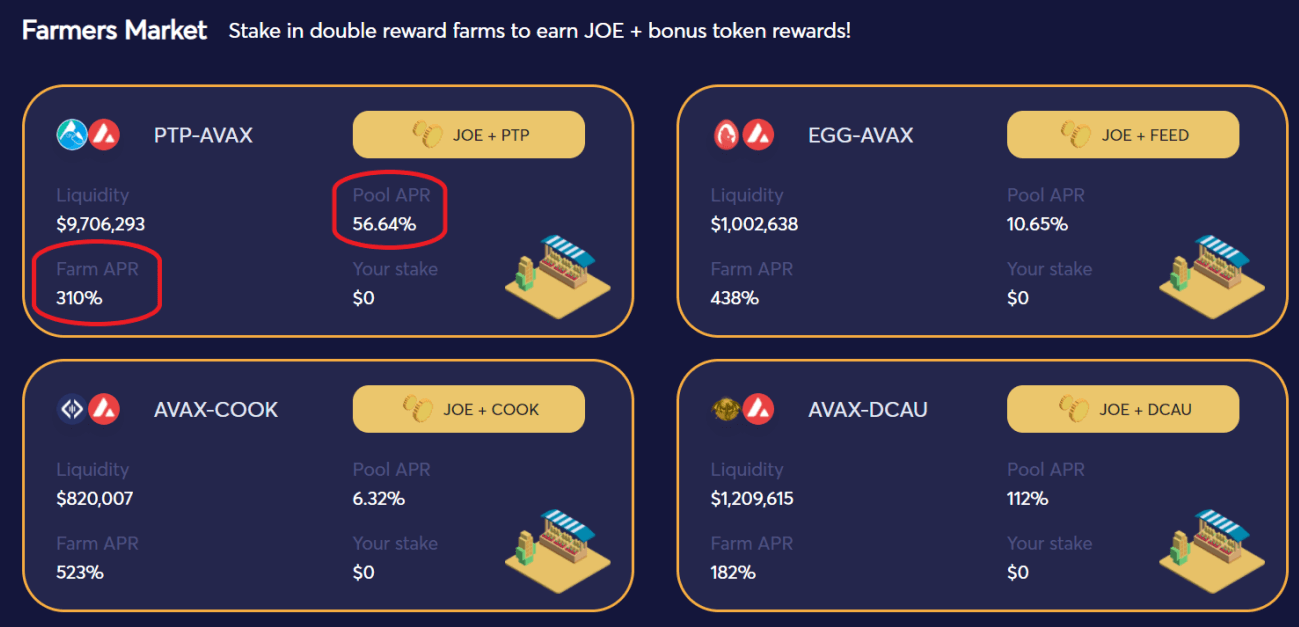

Although both of these terms refer to the return you would get on your deposits, APR does not consider the effect of compounding, while APY does, which is why it is usually much higher than the APR for any investment. Below is the APR for farms on ANX, which highlights both the yield for providing the liquidity, as well as the bonus returns from staking the LP tokens in the corresponding farm.

Assuming your yield is compounded every month, investors could earn interest on top of the interest earned from previous months, resulting in additional yield that can be pretty significant in the long term. If the yield is generated annually, then the APR and APY should be precisely the same.

Depending on the amount of liquidity as well as the trading activity associated with a particular liquidity pool, depositors can usually expect a generous return, even more so if they are particularly early or own a large share of the liquidity pool. But as we’ve mentioned before, impermanent loss is a risk for liquidity providers everywhere, even for the most seasoned yield farmers.

Assuming your yield is compounded every month, investors could earn interest on top of the interest earned from previous months, resulting in additional yield that can be pretty significant in the long term. If the yield is generated annually, then the APR and APY should be precisely the same.

Depending on the amount of liquidity as well as the trading activity associated with a particular liquidity pool, depositors can usually expect a generous return, even more so if they are particularly early or own a large share of the liquidity pool. But as we’ve mentioned before, impermanent loss is a risk for liquidity providers everywhere, even for the most seasoned yield farmers.

What is impermanent loss?

Impermanent loss is incurred when liquidity providers receive different amounts of assets upon withdrawal, compared to when they first deposited them into a liquidity pool on an automated market maker (AMM) such as Uniswap or Sushiswap. This is due to changes in token price, which affects the composition of the liquidity pool, resulting in you having slightly less or more of a particular token. For example, even if you deposited your assets at a 50:50 ratio at the start, there is no guarantee that you will receive the same amount of each asset in the end. This may result in liquidity providers receiving a lower value of assets than if they just chose to hold the tokens in their wallet instead.

How do you calculate impermanent loss?

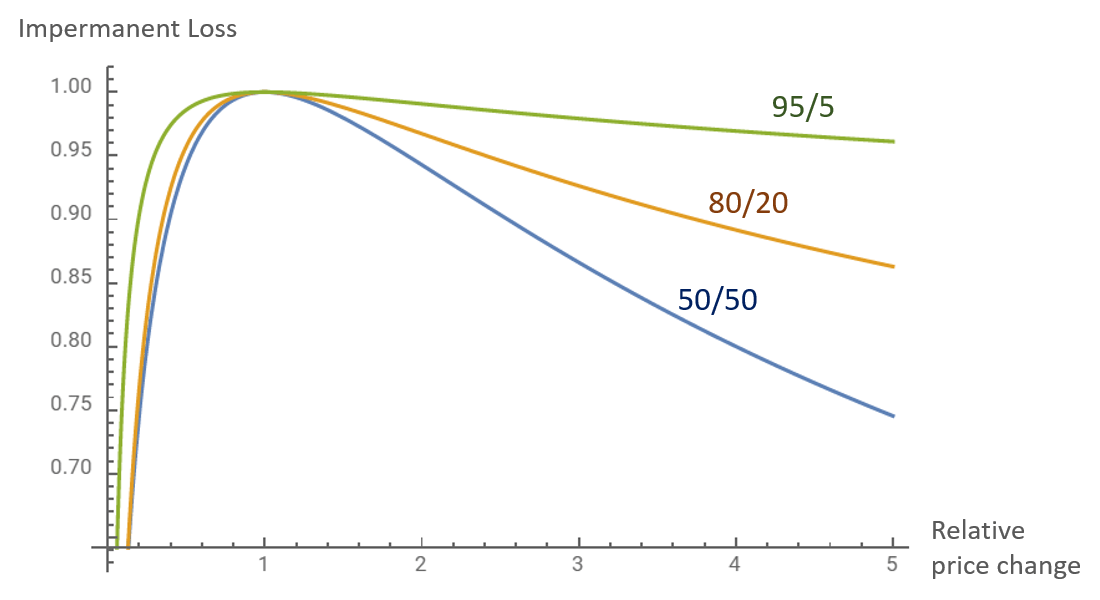

Now that you’ve understood how impermanent loss occurs, how do you calculate exactly how much you’ve lost from providing liquidity? If the price of the assets in a pool changes by a certain amount, the total value of your deposits will be affected, and we can simply plot these results on a graph. Since we are talking about the price change, it does not matter whether the price of the assets goes up or down, as you would still be better off holding the assets instead.

Source: Alex Beckett

Depending on the amount of liquidity as well as the trading activity associated with a particular liquidity pool, depositors can generate a positive return if the earned fees exceed their impermanent loss or not at all. These fees that depositors can expect to receive are usually represented in percentage form, otherwise known as the APY.

Source: Alex Beckett

Depending on the amount of liquidity as well as the trading activity associated with a particular liquidity pool, depositors can generate a positive return if the earned fees exceed their impermanent loss or not at all. These fees that depositors can expect to receive are usually represented in percentage form, otherwise known as the APY.

Or check it out in the app stores

Or check it out in the app stores