Machine learning has become instrumental in the world of algorithmic trading strategies, utilizing numerical, categorical, and ordinal data to build simplified models of the real world. This article will leverage pycgapi, an unofficial Python wrapper for accessing the CoinGecko API, to fetch crucial market data and build an algorithmic trading strategy.

By combining Python's computational capabilities with the rich datasets provided by CoinGecko, we will apply machine learning techniques to develop, test, and implement algorithmic trading strategies in the cryptocurrency space. More specifically, we'll focus on utilizing the unsupervised machine learning algorithm called the Hierarchical Risk Parity (HRP) portfolio strategy.

Prerequisites

In this section, we've outlined the necessary background knowledge, software, and libraries you'll need, as well as steps to set up your environment, to follow along with the tutorial.

Background Knowledge

- Python Proficiency: You should be comfortable with basic programming concepts like variables, loops, and functions, as well as more advanced topics such as working with libraries and handling data.

- Understanding of Financial Markets: A basic understanding of financial markets and instruments, especially cryptocurrencies, will be beneficial.

- Mathematics and Statistics: Knowledge of basic mathematics and statistics is recommended to follow the financial analysis parts of the tutorial.

Google Colab

This tutorial utilizes Google Colab, a free cloud service that allows you to write and execute Python in your browser with zero configuration required, access to free GPUs, and easy sharing. Using Google Colab eliminates the need for local setup and ensures that everyone has access to the same computing environment, making it easier to follow along and troubleshoot.

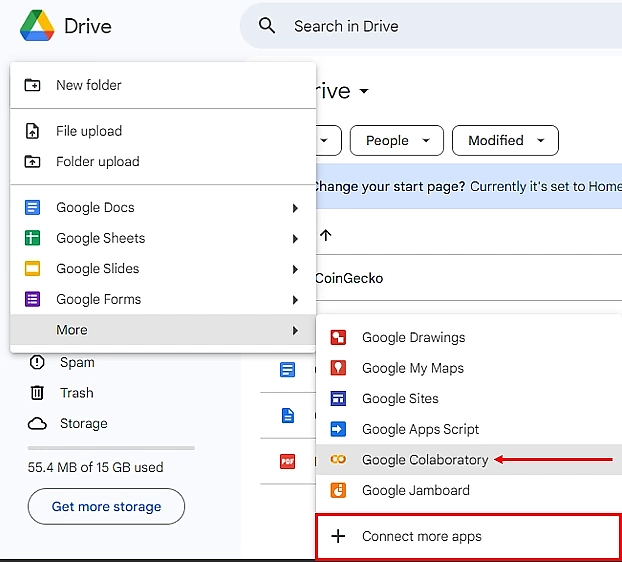

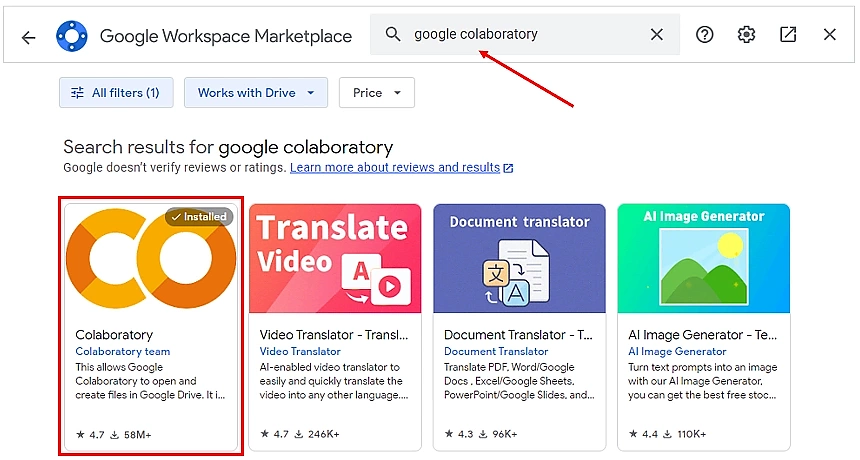

Make sure that Google Colaboratory is added to your Google Drive account's connected apps as you see below. In your Google Drive account, click on '+New' > 'More'. If you do not see Google Colaboratory in the menu, click on '+Connect more apps'.

Search for "Google Colaboratory", and install it.

Configure API Keys

For accessing crypto data and automating trades, we will be using the CoinGecko and Alpaca APIs.

- CoinGecko API: Used to fetch cryptocurrency market data.

- Alpaca API: Enables automated trading on the Alpaca platform.

Setting up your API keys for these services allows us to programmatically retrieve real-time crypto data and execute trades, which are essential components of algorithmic trading. To obtain your API keys:

- Log in to your CoinGecko account and go to the Developer's Dashboard. Click on "Add New Key". Store in a secure location.

- Log in to your Alpaca account and navigate to the Paper Trading Dashboard. Click on "Generate" in the API Keys box. After creation, your API key and secret will be displayed. It's crucial to save these securely at this point, as the secret key will not be shown again. If you lose the secret key, you'll need to generate a new pair.

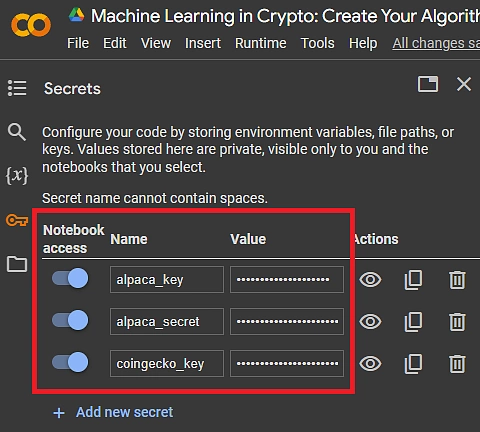

Store API Keys in Google Colab Secrets

In Google Colab, click the key icon in the left side menu.

Enter the name for each key, paste the key as the value, and grant the notebook access to each key.

For accessing financial data, configure your API keys as follows:

Install Required Libraries

This tutorial utilizes several custom Python libraries:

- pycgapi: A client for accessing the CoinGecko API for cryptocurrency data.

- alpaca-py: The official Python library for the Alpaca trading API, enabling automated trading strategies.

- PyPortfolioOpt: Offers portfolio optimization techniques, such as mean-variance optimization.

- bt: A flexible backtesting framework for Python used to test and develop quantitative trading strategies.

Run the following commands in a Google Colab cell to install them:

Import Libraries

Once the installations are complete, import the necessary libraries using the following code. These libraries will help us manipulate data, perform financial analysis, construct portfolios, and run machine learning algorithms.

Initialize API Clients

Now, let's set up the clients needed to interact with the CoinGecko and Alpaca APIs. These clients act as the bridge between our Python code and the external services, allowing us to fetch real-time cryptocurrency data and execute trades programmatically.

For CoinGecko, we'll be using a pro API key due to the amount of data required and to operate with higher rate limits.

For Alpaca, you will need either a paper (simulated trading) or live trading API key, depending on your trading mode preference.

Initialize CoinGecko API Client

To interact with the CoinGecko API, we initialize a client that will make requests for cryptocurrency data. This data is crucial for making informed trading decisions in our algorithm.

CoinGecko API Server Status: {'gecko_says': '(V3) To the Moon!'}

Initialize Alpaca API Client

For executing trades, we use the Alpaca API client. This client will be configured for either paper trading (simulated) or live trading, based on our earlier paper setting.

Alpaca Trading Client Initialized: Paper Trading

Investment Universe

In this section, we align the tradable cryptocurrency tickers from Alpaca with their corresponding coin IDs in CoinGecko. This alignment is crucial because Alpaca and CoinGecko use different formats for cryptocurrency tickers. For example, Alpaca uses currency pairs like "BTC/USD", whereas CoinGecko identifies cryptocurrencies by coin IDs, such as "bitcoin". By reconciling these formats, we ensure our strategy only considers cryptocurrencies that are both tradable on Alpaca and have data available on CoinGecko.

Tradable Crypto Tickers on Alpaca

First, we retrieve all tradable cryptocurrency tickers from Alpaca, focusing on those we can trade and have data for on CoinGecko.

Tradable Currency Pairs on Alpaca:

tradable

symbol

AAVE/USD True

AAVE/USDC True

AAVE/USDT True

AVAX/USD True

AVAX/USDC True

Crypto Tickers from CoinGecko

Next, we match the tradable tickers from Alpaca with CoinGecko coin IDs, excluding those with a base currency of "BTC" to focus on US Dollar-based pairs.

100%|██████████| 56/56 [00:09<00:00, 5.98it/s]

Found CoinGecko IDs for 20 assets.

Collect CoinGecko Coin IDs

We collect the CoinGecko coin IDs from the search results, excluding stablecoins to focus on risky assets.

CoinGecko Coin IDs:

aave

avalanche-2

basic-attention-token

bitcoin

bitcoin-cash

chainlink

curve-dao-token

dogecoin

ethereum

litecoin

maker

polkadot

shiba-inu

sushi

tezos

the-graph

uniswap

yearn-finance

Map CoinGecko Coin IDs to Alpaca Trading Symbols

Finally, we create a mapping between the CoinGecko coin IDs and Alpaca trading symbols for use in subsequent trading logic.

Ticker Mapping:

aave: AAVE/USD

avalanche-2: AVAX/USD

basic-attention-token: BAT/USD

bitcoin-cash: BCH/USD

bitcoin: BTC/USD

curve-dao-token: CRV/USD

dogecoin: DOGE/USD

polkadot: DOT/USD

ethereum: ETH/USD

the-graph: GRT/USD

chainlink: LINK/USD

litecoin: LTC/USD

maker: MKR/USD

shiba-inu: SHIB/USD

sushi: SUSHI/USD

uniswap: UNI/USD

usd-coin: USDC/USD

tether: USDT/USD

tezos: XTZ/USD

yearn-finance: YFI/USD

Fetching Real-time & Historical Crypto Price Data

Use the CoinGecko API to fetch real-time and historical crypto price data. This is essential for the analysis underlying our trading strategy.

Earliest Start Dates

The availability of historical data is assessed to ensure each cryptocurrency in our selection has sufficient historical data for analysis. Use this information to assess whether you should to omit any assets whose earliest start date is too recent.

100%|██████████| 18/18 [00:13<00:00, 1.37it/s]

Earliest Data Start Dates:

the-graph 2020-12-17

aave 2020-10-03

avalanche-2 2020-09-22

uniswap 2020-09-17

sushi 2020-08-28

polkadot 2020-08-19

curve-dao-token 2020-08-14

shiba-inu 2020-08-01

yearn-finance 2020-07-18

tezos 2018-07-03

maker 2017-12-20

chainlink 2017-11-09

bitcoin-cash 2017-08-02

basic-attention-token 2017-06-08

ethereum 2015-08-07

dogecoin 2013-12-15

bitcoin 2013-04-28

litecoin 2013-04-28

Name: Start Dates, dtype: object

Current Prices

We download current market prices for each selected cryptocurrency, providing a current view of market conditions.

Current Prices:

usd

AAVE/USD 102.730000

AVAX/USD 38.930000

BAT/USD 0.270338

BTC/USD 53392.000000

BCH/USD 270.950000

LINK/USD 18.960000

CRV/USD 0.599837

DOGE/USD 0.086983

ETH/USD 3152.620000

LTC/USD 71.140000

MKR/USD 2092.800000

DOT/USD 7.990000

SHIB/USD 0.000010

SUSHI/USD 1.570000

USDT/USD 1.000000

XTZ/USD 1.130000

GRT/USD 0.293909

UNI/USD 10.690000

USDC/USD 1.000000

YFI/USD 8325.900000

Historical Data

We download historical price, market capitalization, and trading volume data for each selected cryptocurrency. This dataset is crucial for analyzing market behavior over the specified period.

100%|██████████| 20/20 [00:12<00:00, 1.63it/s]

Historical Prices:

bitcoin bitcoin-cash chainlink \

timestamp

2022-11-21 00:00:00+00:00 16304.076856 104.914267 5.780015

2022-11-22 00:00:00+00:00 15814.335281 103.401328 5.878893

2022-11-23 00:00:00+00:00 16171.628978 108.902578 6.386520

2022-11-24 00:00:00+00:00 16608.009985 114.523828 6.721798

2022-11-25 00:00:00+00:00 16596.035758 116.688272 6.833340

curve-dao-token dogecoin

timestamp

2022-11-21 00:00:00+00:00 0.512044 0.077732

2022-11-22 00:00:00+00:00 0.501516 0.075124

2022-11-23 00:00:00+00:00 0.633928 0.078690

2022-11-24 00:00:00+00:00 0.688066 0.082338

2022-11-25 00:00:00+00:00 0.689696 0.081835

Categorical Data

Finally, categorical information for each cryptocurrency is collected. This data helps to understand the diversification and exposure of the portfolio across different cryptocurrency categories.

100%|██████████| 20/20 [00:09<00:00, 2.08it/s]

Data Processing

This section outlines the steps to normalize, analyze, and visualize the historical cryptocurrency data, setting a foundation for machine learning analysis.

Normalize Prices for Comparative Analysis

Given the significant price differences across cryptocurrencies, we normalize all prices to start at $1. This approach enables a direct comparison by equalizing the initial investment across all assets.

Compute Historical Returns

We calculate daily and cumulative returns from the normalized prices, which serve as key metrics for evaluating asset performance.

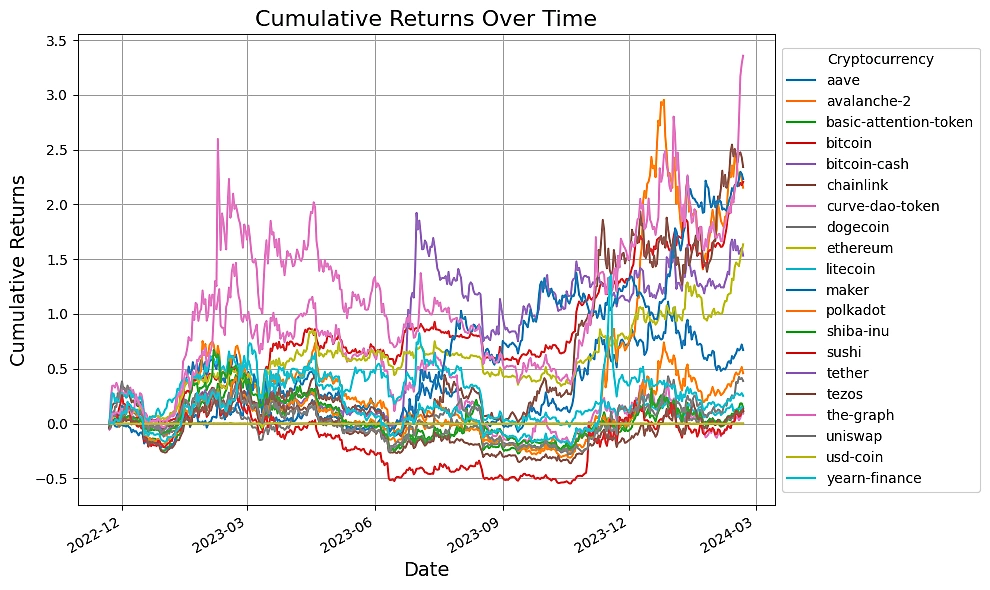

Visualize Cumulative Returns

Visualizing the cumulative returns of selected cryptocurrencies not only brings the data to life but also aids in the identification of standout performers and underperformers within our investment universe.

Prepare Data for Machine Learning

Prior to machine learning analysis, we standardize the historical returns. This normalization ensures that all data features contribute equally to the analysis, improving algorithm performance.

Standardized Historical Returns:

bitcoin bitcoin-cash chainlink curve-dao-token \

timestamp

2022-11-22 00:00:00+00:00 -1.451238 -0.430926 0.357041 -0.492130

2022-11-23 00:00:00+00:00 0.874272 1.263095 2.156707 3.000000

2022-11-24 00:00:00+00:00 1.068304 1.223372 1.276908 1.909221

2022-11-25 00:00:00+00:00 -0.155862 0.403770 0.343712 0.027544

2022-11-26 00:00:00+00:00 -0.314597 -0.667662 0.001589 -0.341132

dogecoin

timestamp

2022-11-22 00:00:00+00:00 -1.023868

2022-11-23 00:00:00+00:00 1.392055

2022-11-24 00:00:00+00:00 1.359091

2022-11-25 00:00:00+00:00 -0.205570

2022-11-26 00:00:00+00:00 2.897963

Algorithmic Trading Strategy: What is Hierarchical Risk Parity (HRP)?

The Hierarchical Risk Parity (HRP) method, introduced in López de Prado (2016), uses hierachical clustering to group assets, not by past returns, but by the similarity in their price series. HRP aims to minimize estimation errors found in conventional portfolio optimization methods by constructing a diversified portfolio that considers the hierarchical relationships between assets. HRP's effectiveness lies in its robustness to market shifts, often outperforming classical diversification techniques.

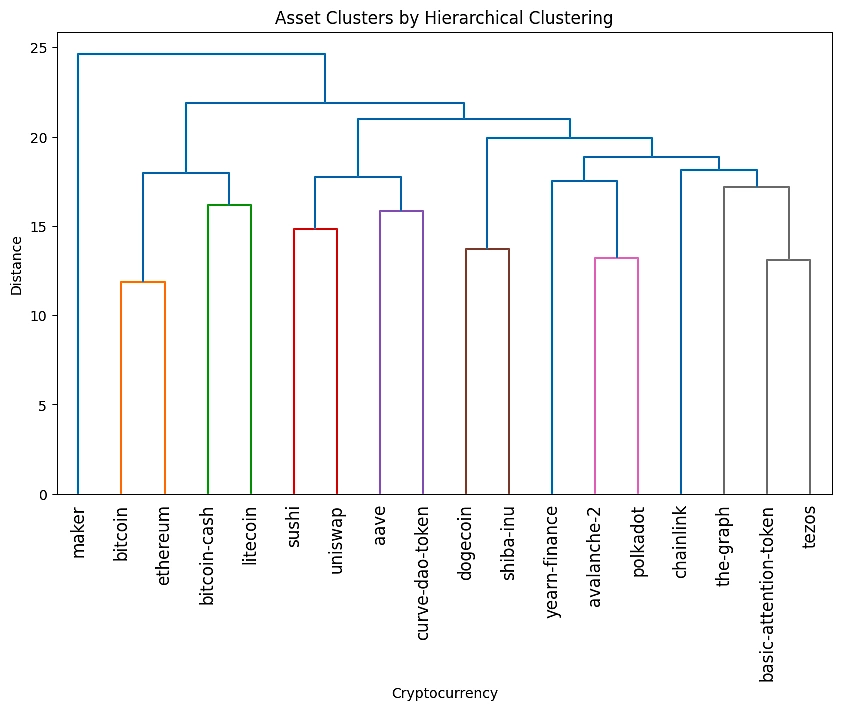

Hierarchical Risk Parity

We start by structuring our assets using hierarchical clustering. This method begins with each asset as a separate cluster and merges them iteratively based on their correlations. The outcome reveals natural groupings in the data, aiding in diversified portfolio construction.

The dendrogram shows how assets link together, with closer branches indicating similar price behaviors. For instance, Bitcoin and Ethereum cluster early, indicating correlated price movements. Conversely, Maker's distinct branch suggests its price behavior is less correlated with the others.

Portfolio Optimization

In the portfolio optimization phase, Hierarchical Risk Parity (HRP) is employed to integrate the clustering results into the asset allocation process. This method accounts for the inherent structure and relationships between assets identified through hierarchical clustering. A crucial step in this process involves computing a risk model using a covariance matrix. The Covariance Shrinkage method, specifically the Ledoit-Wolf shrinkage, is applied to historical returns, which tempers estimation errors by combining the sample covariance with a structured estimator, or "shrinkage target," resulting in a more stable and robust covariance matrix. The HRP model uses this refined covariance matrix to determine the optimal asset weights, aiming for a diversified portfolio that is less sensitive to estimation errors and more attuned to underlying market structures.

HRP Optimized Portfolio:

Optimized Weights

Asset

bitcoin 8.68%

polkadot 7.26%

litecoin 7.14%

ethereum 7.02%

dogecoin 6.85%

tezos 6.74%

shiba-inu 6.58%

uniswap 6.26%

basic-attention-token 6.24%

aave 5.56%

chainlink 5.11%

yearn-finance 4.6%

maker 4.22%

avalanche-2 4.17%

curve-dao-token 3.89%

bitcoin-cash 3.76%

sushi 3.16%

the-graph 2.77%

Expected annual return: 45.7%

Annual volatility: 43.4%

Sharpe Ratio: 1.01

The output of this optimization presents the asset weights guided by the HRP approach and the robust covariance estimation. The performance metrics, which include expected annual return, annual volatility, and Sharpe Ratio, provide a comprehensive view of the portfolio's risk-reward profile.

Categorical Weighting

Finally, we use categorical data to evaluate our portfolio's exposure across various cryptocurrency categories.

Categorical Weights:

Decentralized Finance (DeFi) 35.56%

Smart Contract Platform 34.06%

Layer 1 (L1) 30.37%

Proof of Stake (PoS) 27.96%

Governance 27.68%

Proof of Work (PoW) 26.43%

Meme 13.43%

Layer 0 (L0) 7.26%

Name: Category Weights, dtype: object

Note: Categories can overlap so weights unlikely to total 100%.

The portfolio's largest categorical weighting is in Decentralized Finance (DeFi) at 35.56%, closely followed by Smart Contract Platforms at 34.06%. Both Layer 1 protocols and Proof of Stake mechanisms also hold significant weights, emphasizing the portfolio's tilt towards foundational blockchain technologies and governance systems.

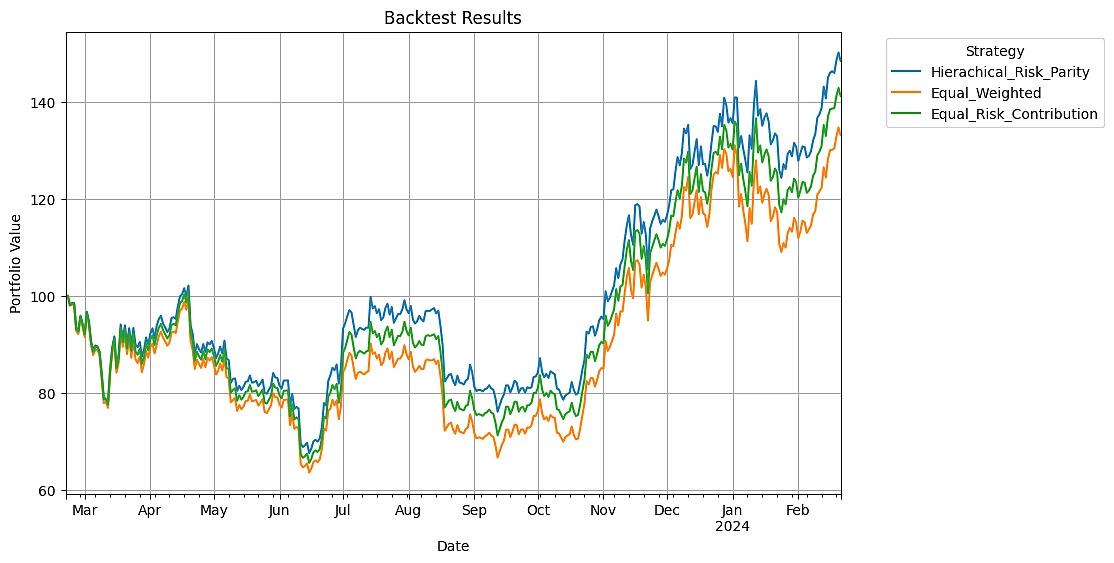

Backtesting Strategy

Backtesting is a crucial step in evaluating the performance of any trading strategy. It allows us to simulate how the strategy would have performed in the past, providing insights into potential future performance. This section outlines the backtest of a Hierarchical Risk Parity (HRP) strategy against other benchmark strategies, including Equal Weighted (EW), Equal Risk Contribution (ERC), and Monte Carlo simulation of randomly generated portfolios.

Strategy Logic

Hierarchical Risk Parity (HRP) Strategy

The HRP strategy aims to optimize asset allocation by considering the hierarchical structure of asset correlations, thus potentially reducing portfolio volatility and improving returns. The WeighHRP class, defined below, implements this strategy by selecting assets and rebalancing the portfolio based on a lookback period.

Equal Risk Contribution (ERC) Strategy

The ERC strategy seeks to allocate portfolio weights in a way that each asset contributes equally to the portfolio's risk, aiming for a more balanced risk distribution across assets.

Backtest Engine

The backtest engine simulates the performance of these strategies over a specified period. It uses historical price data to execute trades according to each strategy's logic and calculates the portfolio's value over time.

Run the Backtest

To initiate the backtest, we set the number of simulations for random portfolios and the lookback period for rebalancing.

The risk-free rate is also defined to calculate the excess return used for risk-adjusted performance.

[*********************100%%**********************] 1 of 1 completed

Average Risk-Free Rate: 3.95%

Run all backtests and plot the performance results of a $100 starting value portfolio for each backtest.

100%|██████████| 3/3 [00:01<00:00, 2.23it/s]

100%|██████████| 1/1 [00:00<00:00, 7345.54it/s]

100%|██████████| 1/1 [00:00<00:00, 10866.07it/s]

100%|██████████| 1/1 [00:00<00:00, 11214.72it/s]

100%|██████████| 1000/1000 [02:17<00:00, 7.29it/s]

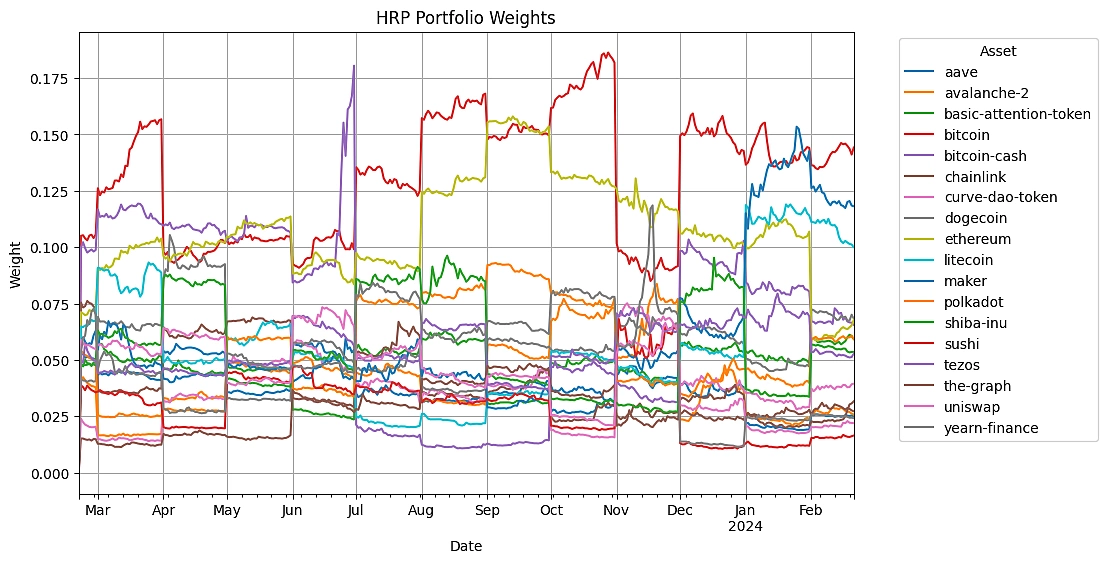

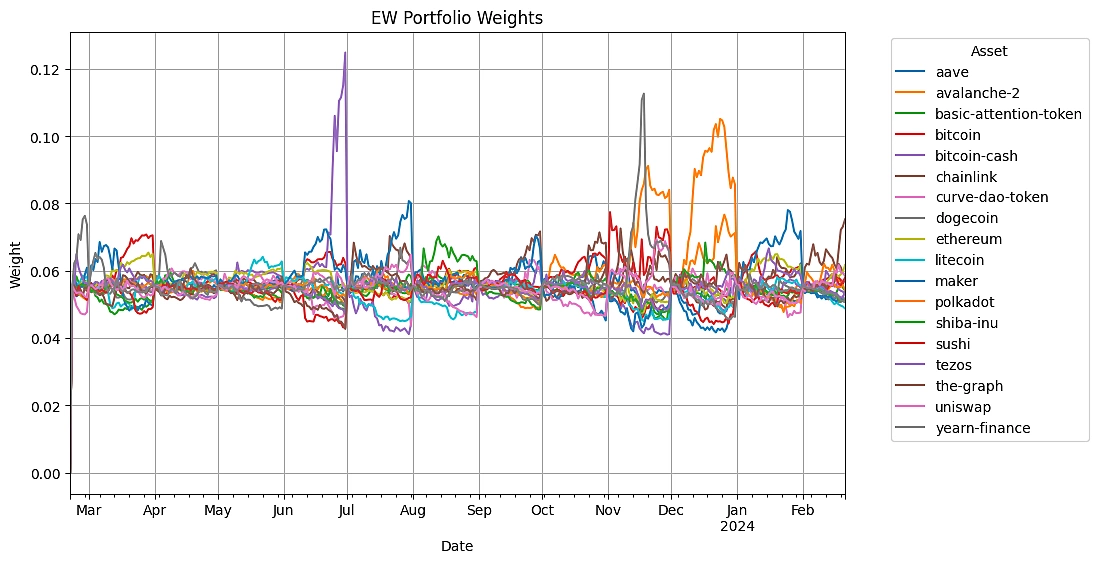

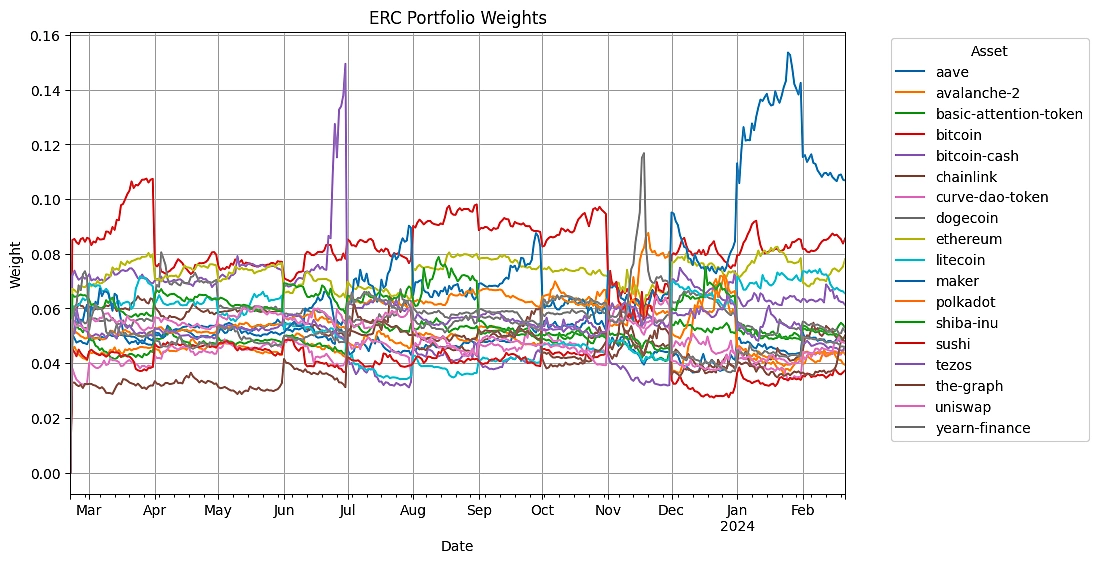

Plot Security Weights

Visualizing the weight allocations over time provides insights into how each strategy changes to market conditions. It helps in understanding the diversification and risk management approach of each strategy.

Backtest Results

After running the backtests, we compile and display the performance statistics for each strategy. This includes measures such as total return, annualized return, maximum drawdown, Sharpe ratio, and others. Comparing these metrics across strategies helps in evaluating their relative performance and risk characteristics.

Backtested Portfolios:

- HRP: Hierarchical Risk Parity

- EW: Equal Weighted

- ERC: Equal Risk Contribution

- ARP: Aggregate Random Portfolio

|

HRP |

EW |

ERC |

ARP |

|---|---|---|---|---|

Start |

2023-02-20 |

2023-02-20 |

2023-02-20 |

2023-02-20 |

End |

2024-02-21 |

2024-02-21 |

2024-02-21 |

2024-02-21 |

Risk-free rate |

3.95% |

3.95% |

3.95% |

3.95% |

Total Return |

48.35% |

33.08% |

41.14% |

33.06% |

CAGR |

48.23% |

33.00% |

41.05% |

32.96% |

Max Drawdown |

-33.78% |

-36.41% |

-34.94% |

-43.75% |

Calmar Ratio |

1.43 |

0.91 |

1.17 |

0.89 |

MTD |

13.56% |

15.68% |

14.39% |

15.95% |

3m |

31.77% |

30.82% |

31.19% |

31.46% |

6m |

76.87% |

80.28% |

79.53% |

81.93% |

YTD |

8.63% |

5.53% |

7.50% |

5.77% |

1Y |

48.35% |

33.08% |

41.14% |

33.06% |

Since Incep. (ann.) |

48.23% |

33.00% |

41.05% |

32.96% |

Best Day |

9.36% |

9.23% |

9.16% |

15.85% |

Worst Day |

-9.39% |

-9.93% |

-9.68% |

-12.25% |

Monthly Sharpe |

1.25 |

0.91 |

1.08 |

0.64 |

Monthly Sortino |

3.18 |

2.16 |

2.58 |

2.03 |

Monthly Mean (ann.) |

53.01% |

44.69% |

49.09% |

44.56% |

Monthly Vol (ann.) |

39.36% |

45.00% |

41.97% |

56.57% |

Monthly Skew |

0.02 |

0.11 |

0.04 |

0.64 |

Monthly Kurt |

-1.46 |

-1.46 |

-1.37 |

0.23 |

Best Month |

20.41% |

22.63% |

21.89% |

36.18% |

Worst Month |

-13.34% |

-15.81% |

-14.99% |

-17.08% |

Avg. Drawdown |

-7.82% |

-7.39% |

-8.17% |

-20.19% |

Avg. Drawdown Days |

22.40 |

28.75 |

22.53 |

101.14 |

Avg. Up Month |

12.09% |

12.53% |

12.13% |

16.29% |

Avg. Down Month |

-6.33% |

-8.61% |

-7.17% |

-9.36% |

During the one-year sample period from February 20, 2023, to February 21, 2024, the Hierarchical Risk Parity (HRP) strategy outperformed the Equal Weighted (EW), Equal Risk Contribution (ERC), and Aggregate Random Portfolio (ARP) strategies in terms of total return, with HRP achieving a 48.35% return. It also exhibited a Compound Annual Growth Rate (CAGR) of 48.23% and a maximum drawdown of -33.78%. While the HRP strategy showed a notable Calmar Ratio of 1.43 and the highest Monthly Sharpe Ratio of 1.25 among the strategies, indicating a favorable risk-adjusted return during the sample period, it is important to recognize that these results are specific to the timeframe analyzed. The performance of the HRP strategy, compared to the others, underscores its effectiveness in this particular context without necessarily implying overall superiority across all market conditions or time periods.

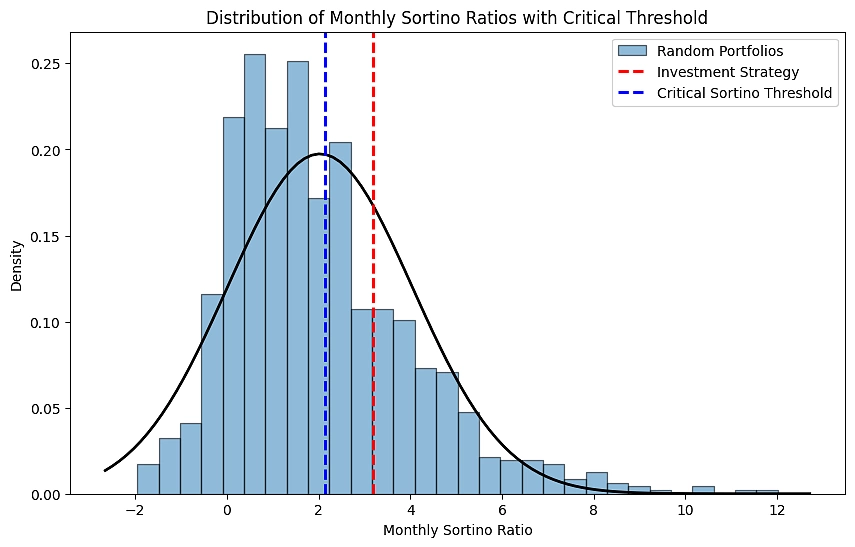

Monte Carlo Hypothesis Test

In the hypothesis test, we are examining whether the Hierarchical Risk Parity (HRP) strategy's performance, as measured by the monthly Sortino ratio, is significantly better than what could be expected by random chance from a selection of portfolios. The null hypothesis (H0) and alternative hypothesis (Ha) are defined as follows:

H0: Strategy's return ≤ 1,000 random portfolios. (μstrategy ≤ μrandom)

Ha: Strategy's return > 1,000 random portfolios. (μstrategy > μrandom)

Here, μstrategy is the mean monthly Sortino ratio of the investment strategy, and μrandom is the mean monthly Sortino ratio of the random portfolios.

Result: The portfolio outperformed the sample of randomly generated portfolios.

T-statistic: 18.0693

P-value (one-tailed): 0.0000

Significance Level: 0.05

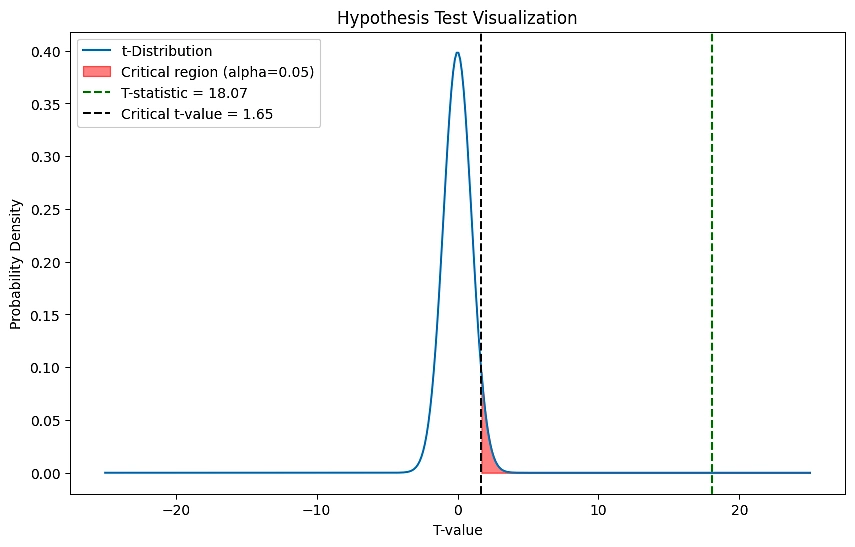

Upon running the test, the results display a p-value of 0.0000 and a t-statistic of 18.0693. If we reject the null hypothesis, we are asserting that there is sufficient evidence to claim that the investment strategy has outperformed the random portfolios with a confidence level of 95%. The plot further substantiates this finding, showing the investment strategy's Sortino ratio significantly to the right of the critical Sortino ratio threshold and the distribution of the random portfolios.

The plot visualizes the results of the hypothesis test for the Hierarchical Risk Parity (HRP) strategy's performance. The blue curve represents the t-distribution of t-values obtained from the Monte Carlo simulation. The red shaded area to the right of the black dashed line signifies the critical region for our alpha level of 0.05, where any t-statistic falling within this region would lead us to reject the null hypothesis. Our observed t-statistic, indicated by the green dashed line, falls well within the critical region, affirming that the HRP strategy's performance is statistically significantly greater than that of the random portfolios. The critical t-value of 1.65 is the threshold above which we reject the null hypothesis, and our t-statistic of 18.07 vastly exceeds this, providing strong evidence against the null hypothesis in favor of the alternative.

Automating Strategy

This section introduces a trading bot that automatically executes the Hierarchical Risk Parity strategy, converting targeted allocations into market orders while managing existing positions and respecting minimum trade thresholds. The bot also features a preview mode to validate trades before execution.

Trading Bot

The function create_positions_dataframe converts the account positions into a Pandas DataFrame. This standardized format is essential for the trading bot to assess current holdings against target allocations.

The preview_mode flag allows users to test the trading bot without executing real trades, providing a safeguard and a means to validate the bot's logic before live operation. If preview_mode is set to False, then the trading bot will execute live orders. Use with caution.

The min_trade_value is set to $100, indicating that the bot will ignore any trades below this amount to ensure that transactions are economically viable.

Here we initialize our trading bot, fetching current account details and holdings. It assesses the portfolio's value, cash availability, and buying power. Based on the optimized weights from our strategy, the bot prepares a list of trades, considering the minimum trade value threshold to avoid executing economically insignificant trades. The trading bot then simulates the execution of these trades, providing an overview of buy and sell orders. This simulation allows for a final review before live trading, ensuring alignment with our strategy and capital allocation rules.

Starting Trading Bot...

Portfolio Value: $102,198.99

Cash: $14,678.53

Buying Power: $29,357.06

Account Holdings:

qty side market_value cost_basis

symbol

AAVE/USD 53.031986 PositionSide.LONG 5449.036580 4873.639530

AVAX/USD 56.150439 PositionSide.LONG 2166.845424 2175.267990

BAT/USD 13704.653261 PositionSide.LONG 3705.436739 3453.435575

BCH/USD 20.679385 PositionSide.LONG 5605.560950 5374.841049

BTC/USD 0.304311 PositionSide.LONG 16271.957289 15619.655041

CRV/USD 10941.174129 PositionSide.LONG 6583.960944 0.000000

DOGE/USD 34293.311273 PositionSide.LONG 2987.156601 2956.426365

DOT/USD 463.152266 PositionSide.LONG 3719.112695 0.000000

ETH/USD 2.761884 PositionSide.LONG 8713.744512 8071.661684

GRT/USD 7204.676907 PositionSide.LONG 2120.480507 1720.671372

LINK/USD 277.058115 PositionSide.LONG 5253.215799 5090.194804

LTC/USD 101.623754 PositionSide.LONG 7216.099548 7009.420266

SUSHI/USD 2899.258768 PositionSide.LONG 4541.109008 3664.692075

UNI/USD 682.816928 PositionSide.LONG 7777.284814 5011.261719

XTZ/USD 4775.295230 PositionSide.LONG 5409.454436 0.000000

Preparing Trades...

100%|██████████| 18/18 [00:00<00:00, 4038.16it/s]

Previewing Trades...

Preview sell order for BTC/USD: Notional $7,400.06

Preview sell order for ETH/USD: Notional $1,535.29

Preview sell order for UNI/USD: Notional $1,379.63

Preview sell order for CRV/USD: Notional $2,612.51

Preview sell order for BCH/USD: Notional $1,760.83

Preview sell order for SUSHI/USD: Notional $1,314.69

Preview buy order for DOT/USD: Notional $3,700.53

Preview buy order for DOGE/USD: Notional $4,011.43

Preview buy order for XTZ/USD: Notional $1,474.67

Preview buy order for SHIB/USD: Notional $6,725.72

Preview buy order for BAT/USD: Notional $2,669.74

Preview buy order for AAVE/USD: Notional $231.18

Preview buy order for YFI/USD: Notional $4,696.04

Preview buy order for MKR/USD: Notional $4,313.82

Preview buy order for AVAX/USD: Notional $2,091.79

Preview buy order for GRT/USD: Notional $711.45

Total Trades: 16

Sell Trades: 6

Buy Trades: 10

Done!

The trading bot initiation displays a portfolio valued at $102,198.99, with $14,678.53 in cash and $29,357.06 available for buying power. The current account holdings are diversified across various cryptocurrencies, with Bitcoin holding the highest market value in the portfolio. The bot is set to preview 16 trades, consisting of 6 sells and 10 buys, with transactional decisions based on optimizing portfolio weightings. Notably, the largest intended transaction is a sell order for Bitcoin at a notional value of $7,400.06, demonstrating the bot's capability to handle significant trade volumes. The trade previews successfully conclude the session, signaling readiness for actual execution pending confirmation.

Risks, Considerations & Conclusion

Algorithmic trading, while offering numerous benefits such as speed, efficiency, and the elimination of emotional decision-making, comes with its own set of risks and considerations. A key risk involves the potential for overfitting, where a strategy might perform exceptionally well on historical data but fails to predict future movements accurately. This is particularly pertinent to machine learning-based strategies like Hierarchical Risk Parity (HRP), which may capture noise as a signal if not properly validated.

The allure of machine learning in finance can sometimes overshadow the inherent limitations of these algorithms. It's crucial to maintain a scientific level of skepticism towards any trading strategy, regardless of its complexity or the sophistication of the algorithms involved. The success of machine learning models, including HRP, depends heavily on the quality and relevance of the data they are trained on, and their performance can be significantly impacted by market conditions, structural changes in the economy, or regulatory environments.

Trading bots, although powerful, operate under the constraints of their programming. They lack the human capacity for judgment and context-based decision-making, which can sometimes lead to unintended trades or failure to adapt to new market conditions. Additionally, technical issues such as connectivity problems, system crashes, or software bugs can result in missed trades or duplicate orders. Moreover, financial markets are influenced by a myriad of factors that are difficult to quantify, such as political events, changes in consumer behavior, or the emergence of new technologies. These elements can lead to situations that a machine learning model or trading bot has never encountered, potentially leading to suboptimal decisions.

In conclusion, while machine learning and algorithmic trading strategies like HRP can be valuable tools for investors, they should not be viewed as infallible solutions. Traders must exercise due diligence, continuous monitoring, and rigorous backtesting against out-of-sample data to ensure that these strategies remain robust under various market conditions. It is also vital to have risk management protocols in place to mitigate potential losses when the strategies do not perform as expected.

Disclaimer

The information provided in this article, including but not limited to text, graphics, code examples, and any other material, is for educational and informational purposes only. It is not intended as, and should not be construed as, financial advice, investment recommendation, or an endorsement of any particular security, strategy, or investment product. The article discusses concepts related to algorithmic trading strategies in the context of cryptocurrency markets using machine learning techniques. The examples and strategies outlined are provided to illustrate the application of machine learning in analyzing cryptocurrency data and do not constitute advice on investing or trading in cryptocurrencies or any other assets. The strategies and examples presented are purely hypothetical and are not guarantees of future performance or success. Investing and trading in cryptocurrencies involve significant risk, including the potential loss of principal. Market conditions, economic factors, and the volatile nature of cryptocurrencies can affect investment outcomes. Readers are strongly encouraged to conduct their own research and consult with a qualified financial advisor or investment professional before making any investment decisions. The author and publisher of this article are not responsible for any financial losses or damages resulting from the application of the information provided.

Looking for more crypto algorithmic trading guides that leverage Python? Check out this article that focuses on artificial neural networks in crypto algo trading.

```

Or check it out in the app stores

Or check it out in the app stores