General Risks for All Stablecoins

Crypto stablecoins are a type of cryptocurrency that aims to maintain a stable value relative to a target asset, such as a fiat currency or a commodity. This is achieved through a variety of mechanisms, including fiat collateralization, algorithmic stabilization, and hybrid models. However, no stablecoin design is perfect (up to now) - each comes with its own risk, and indeed, over time we have seen events of stablecoin depeg occur, sometimes to disastrous effects for its users. In this article Reflexivity Research identifies the key risk areas underlying each stablecoin design.

Key Takeaways

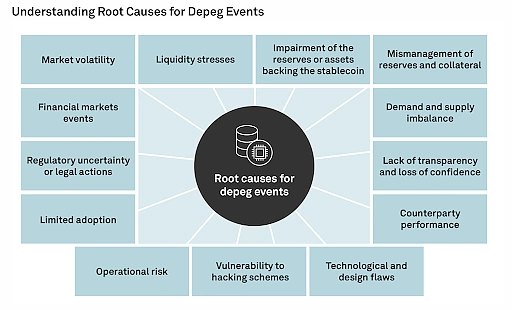

- Given that the main function of a stablecoin is for its value to remain stable to a certain fiat curency or asset, the biggest risk is for it to display unstable prices, or even a complete depeg from the actual asset prices. The root causes of depeg events can come be due to external factors, e.g. changes to interest rates, regulatory issues, or internal factors, e.g. hacking, redemption / arbitrage risk, etc.

- Centralized, fiat-collateralized stablecoins still command the most market share amongst stablecoins, with USDT and USDC being the most prominent examples. All of these stablecoins come with a degree of centralization risk, as they operate under the control of regulated, profit-driven entities that have the authority to mint new coins and freeze existing assets. Users also have to depend on either disclosures from the entity, or audits to have a view of the reserves backing the stablecoin.

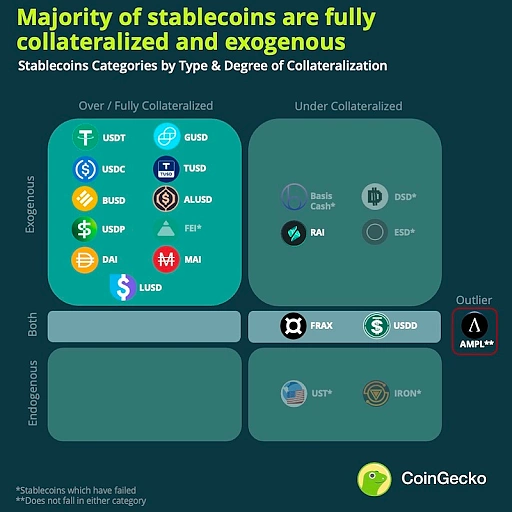

- For algorithmic stablecoins, they carry the risk of all exogenous stablecoins, but also has an additional risk of endogenous collateral that is susceptible to increased reflexivity in volatile markets. The collapse of Terra's UST stablecoin in 2020 is a prime example of this risk, as it was mainly backed by Terra's own governance token, LUNA. With endogenous collateral, a significant decrease in value can also destabilize the stablecoin, triggering a "death spiral" for both assets.

Price Stability / Depeg Risk

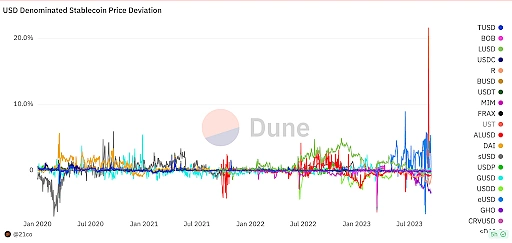

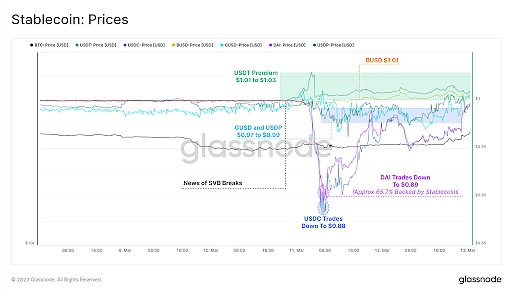

Despite the moniker of “stablecoins,” these crypto assets are not immune to market and external pressures. They can, and do, deviate from their targeted value, usually $ 1 USD (image below). Such events are often a culmination of microeconomic factors like sudden demand surges, liquidity challenges, or alterations in the foundational collateral.

A chart simply illustrating that stablecoins rarely trade at exactly $1. Source

Macro events, like inflationary trends or interest rate amendments, can equally sway stablecoin demand. Consider an inflationary environment where the underlying asset's purchasing power dwindles. This can compel the stablecoin to depeg.

Externalities, such as regulatory headlines or even technical snafus like network congestion or smart contract vulnerabilities, can also be catalysts. A government's decision to prohibit stablecoins, for instance, would severely dent demand, instigating a depegging event.

Smart Contract Risk with the Stablecoin Protocol

Fully autonomous, smart contracts removing middlemen and operating without bias sounds great but only if the code is safe. Using stablecoins on a blockchain means users not only need to be sure the actual blockchain is safe but also the project responsible for the stablecoin. Unfortunately, that is not always the case as Level Finance experienced in 2023. Level Finance, a DeFi protocol that issues an interest-bearing stablecoin, lost $1 million due to a glitch in its smart contract.

The core of the issue lay in a flaw that permitted the nefarious attacker to produce an excessive quantity of LUSD stablecoins without the mandated collateral backup. Essentially, the attacker could mint these stablecoins at will, subsequently trading them for other digital assets, thereby illicitly extracting value from the Level Finance ecosystem.

Other Risks and Considerations

-

Token Centralization/Governance Risk

-

Liquidity Centralization (e.g. primarily all-in-one liquidity pool)

-

Supply Constraints: is the growth of the stablecoin dependent on the growth of another sector (RWAs, decentralized futures, LSTs, etc.)

-

Redemption/Arbitrage Risk: inefficient redemption mechanisms may impede the stablecoin design from functioning as designed

-

Integrations into Other Protocols/Contagion Risk: the MIM-UST “Degenbox” Scare

Risks of Centralized, Fiat-collateralized Stablecoins

Centralization and Censorship

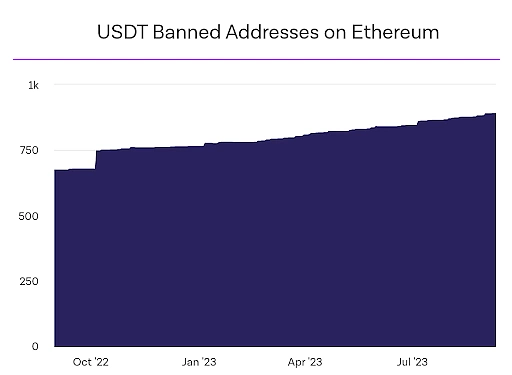

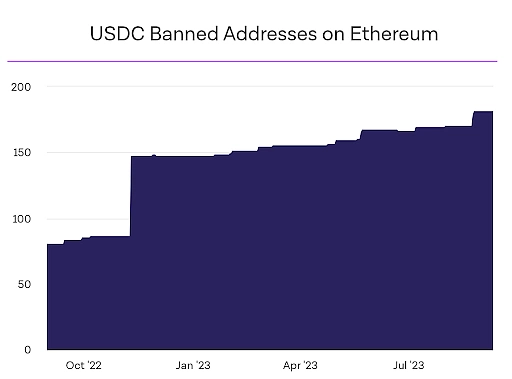

In an almost paradoxical fashion, the two leading stablecoins in the crypto space, USDT and USDC, embody a significant degree of centralization and counterparty risk. Every stablecoin displays some mixture of centralized and decentralized features. However, USDT and USDC stand out as they operate under the control of regulated, profit-driven companies that possess the authoritative power to mint new coins and, quite notably, freeze existing assets. Both projects have, on dozens of occasions, "blacklisted" addresses and frozen the funds held within them, something inconceivable to the average person’s understanding of “crypto.”

Source: TheBlock

Unfortunately, many of the people who could stand to benefit from access to USDT or USDC due to their own fiat money being subjected to high inflation, instability, or capital controls are the targets of these asset freezings simply because of their home government’s relationship with the US. Citizens of countries like Iran, Syria, and Venezuela suffer from some of the highest inflation in the world (image below) but also find themselves cut off from USDT and USDC due to US sanctions against those countries. Because of this, these centralized, fiat-backed stablecoins do not pose a solution for people like them, illustrating the value in something like a truly decentralized, crypto-native stablecoin or crypto asset.

Additionally, due to their design, users of USDT and USDC must put 100% faith into Tether and Circle, respectively, to properly manage the hundreds of billions of dollars across the globe in real time. Should either company mismanage its global operation, the ramifications would be felt across the entire crypto economy.

Exogenous Collateral, Reserve Composition, and Transparent Audits

The collateral backing a protocol's stablecoin can be categorized as either endogenous or exogenous in nature. Endogenous assets, in this context, are crypto tokens intrinsically linked to the protocol, serving roles like equity or governance (akin to LUNA in the Terra and UST ecosystem). Conversely, ETH represents an exogenous crypto asset, which is often viewed as a more desirable form of collateral because its value remains independent of the protocol's progress and longevity. The US dollar would be ever more exogenous as it is not a crypto asset and has even less correlation to the underlying stablecoin.

For these fiat-backed stablecoins, the crux of investor confidence often hinges on the clarity of their financial health and operations.

While many might assume that a "USD-collateralized" label signifies a one-to-one backing by the US dollar, the reality is more nuanced as the collateral backing these stablecoins is typically diversified into an array of assets. These might include cash equivalents such as US treasuries and commercial paper, but also encompass secured loans, and corporate bonds, among others.

Acknowledging the importance of transparency in this domain, there has been a concerted push towards enhancing clarity and reporting mechanisms for USD-collateralized stablecoins. Moody's, a renowned TradFi credit rating agency, is even devising a scoring methodology tailored for fiat-backed stablecoins. This system aims to assess these digital assets based on the robustness of their reserve attestations.

Circle's USDC, one of the prominent stablecoins in the market, has bolstered its commitment to transparency, releasing monthly reports detailing its reserves with attestations from Grant Thornton, a globally recognized accounting firm.

Regrettably, when it comes to Tether, transparency into its reserve composition and internal operations poses challenges for investors and users alike. While many financial institutions and companies in today's era leverage technology to provide real-time updates on their balance sheets, Tether is seemingly incapable of doing so. The company's balance sheet data is updated quarterly, a cadence that might have been standard in traditional finance, but in the rapidly moving digital currency ecosystem, could be seen as outdated. This periodicity leaves a considerable gap where market movements can happen, and investors are left in the dark.

Furthermore, these quarterly reports, though informative, still leave many pertinent questions unanswered. For the astute reader, these reports lack clarity on several fronts:

-

Financial Institution Partnerships: The identity of the financial institutions that hold Tether's cash deposits remains undisclosed. The geographical location of these institutions is equally unclear. Knowing the "who" and "where" can give investors insights into the financial stability, regulatory environment, and potential risks associated with these holdings.

-

Foreign Treasury Details: While Tether's holdings in U.S. Treasury Bills might be known, details about non-U.S. Treasury Bills remain undisclosed.

-

Interest Rate Exposure: The interest rate risk associated with many of Tether’s assets (and possibly some of USDC’s) is not completely known. As interest rates have exhibited extreme volatility over the last ~two years, this becomes more significant to the reserves held by each entity.

-

Loan Terms and Collaterals: Details about the terms of secured loans taken by Tether, as well as the collateral backing these loans, are missing. Such details can provide a deeper understanding of the company's credit risk and the safety of its financial position.

Other potential hazards for USDT and USDC users include:

-

Fluctuations in the U.S. dollar value.

-

Uncertainties surrounding U.S. Treasuries.

-

Possibility of bank runs.

-

Improper risk mismanagement of funds or banking partners.

-

Internal mismanagement or even malicious practices by the overseeing company.

Banking/Counterparty/Custody Risk

Because USDT and USDC are (essentially) digital representations or IOUs of the U.S. dollar, this brings forth another layer of centralization/risk: custodying the fiat collateral that backs the stablecoin. The onus of safeguarding these funds and ensuring their seamless transfer falls upon their banking partners and all the problems/frictions involved in traditional banking. Consequently, any turbulence - operational glitches, financial insolvency, or even unethical practices - encountered by these partners can create ripples, disturbing the very foundation of these stablecoins.

Despite the risks explained above, many still feel comfortable holding USDT and USDC, acknowledging that the risks sound no different than standard banking risks. And they would be correct to a certain extent. Plus, with such a large, reputable, and regulated company behind USDC like Circle, users assume extra protections that other stablecoins can offer, like insurance. However, while users might derive a sense of security from insurance mechanisms like the Federal Deposit Insurance Corporation (FDIC), digging into the details of Circle’s recent practices illustrates how little protection users actually had in the event of a crisis. As Circle's 2021 data suggests, out of the staggering $10 billion parked in regulated financial institutions, a mere ~$1.75 million was under the protective umbrella of FDIC ("Circle Internet Financial Limited"). In the unfortunate event of a bank collapse, USDC holders could find themselves vying with other claimants for their due.

The reality was that a significant chunk of USDC's backing cash was vulnerable, lying beyond the FDIC's $250,000 insurance ceiling when it suffered banking issues in March 2023. Silicon Valley Bank ran into solvency issues and assets held at the bank were at risk. This caused USDC to depeg as ~8% of the US dollars backing the stablecoin were potentially unrecoverable.

Regulatory Risk

Centralized stablecoins, in particular, have recently become a prominent focus for regulatory bodies, as evidenced by recent actions and proposals. One of the most noteworthy instances of this regulatory spotlight involves Paxos Trust (Paxos). The New York Department of Financial Services (NYDFS) initiated action against Paxos in 2023, instructing them to cease Binance USD (BUSD) issuance. The crux of NYDFS's contention was Paxos’s purported negligence in its duty to carry out consistent risk assessments.

Further intensifying the scrutiny, the Securities and Exchange Commission (SEC) advanced its allegations against Paxos, suggesting that BUSD qualifies as a security through its Wells Notice. While the immediate repercussions of these actions only pertain to BUSD, it is evident that centralized stablecoins, by extension, are vulnerable to significant regulatory interventions.

Further evidence for the growing regulatory concerns around stablecoins was the introduction of the STABLE Act in December 2020. The essence of this act is anchored in the objective of thwarting potential malfeasance, lack of transparency, and the speculative emergence of a stablecoin-driven shadow banking system.

However, the requirements proposed are seen by many as particularly onerous, to the point of potentially killing off current stablecoin designs/issuers. If the act were to be ratified, stablecoin issuers would find themselves navigating the almost impossible requirements of:

-

A necessity to procure a federal banking charter.

-

An obligation to gain endorsements from both the Federal Reserve and the Federal Deposit Insurance Corporation (FDIC), and this, a full half-year prior to any stablecoin issuance.

-

An additional stipulation to either secure FDIC insurance or establish dollar reserves directly within the Federal Reserve's precincts.

The intersection of stablecoin innovation and regulatory oversight is becoming increasingly pronounced. For stablecoin issuers, the current unclear regulatory environment leaves them unsure of how to grow while maintaining compliance. As the crypto industry and regulators continue their discussions, the hope is for a balanced approach that ensures both security and innovation.

Oracle Dependence/Centralization

At their core, oracles compile pricing data on assets from a multitude of sources, which CDP-backed stablecoins use in their protocols' stability mechanisms. These digital entities take on the pivotal task of ensuring the stability and reliability of the system, particularly during unpredictable market fluctuations and unforeseen black swan occurrences. The pivotal role oracles play becomes evident when considering the mechanics of crypto loans: for each loan extended, the value of the collateral must maintain a certain threshhold. Should an oracle indicate that a user's collateral-to-loan ratio dips beneath a pre-determined mark, the collateral deposited in the associated smart contract can be mobilized and liquidated to square off the corresponding stablecoins.

Such mechanisms are integral to both Collateralized Debt Positions (CDP) and Algorithmic stablecoins. Consequently, the selection of an oracle solution isn't a decision that should be taken lightly by the protocol. Factors that need meticulous consideration while opting for an oracle include:

-

The oracle's capacity, reliability, and frequency in which it provides price feeds for the specific types of collateral in question, such as ETH, wstETH, or USDC.

-

Its compatibility with both Layer 1 and Layer 2 Networks

-

The inherent transparency, security, decentralization, and accuracy of the price feeds, along with the reliability of their sources.

An oracle exploit occurs when an oracle reports inaccurate data about an event or state of the external world. This can happen because the oracle purposefully acts maliciously or negligently, or the oracle’s data source is compromised.

There are two main types of oracle exploits:

-

Misreporting: This is when an oracle reports a price that differs from the correct market-wide price of an asset. Regardless of whether misreporting occurs due to malicious or negligent behavior, any protocol relying on a faulty oracle for price data may be at risk of an exploit.

-

Poor market coverage: This is when an oracle relies on only a subset of all trading environments to report the price of an asset. This can lead to the oracle misreporting the price of an asset if that subset is manipulated, even when the majority of trading environments and the market-wide price remain unaffected.

The risk of oracle exploits can be mitigated with a more secure oracle design. Features of secure oracles include:

-

Sourcing price data from across all trading environments to provide proper market-wide coverage: This helps to ensure that the oracle is not vulnerable to price manipulation in a single trading environment.

-

Protections from external tampering: This can be achieved by decentralizing the oracle or by using other security measures to prevent unauthorized access to the oracle's data.

-

Economic incentives to report faithfully: This can be achieved by rewarding oracles for reporting accurate data and penalizing them for reporting inaccurate data.

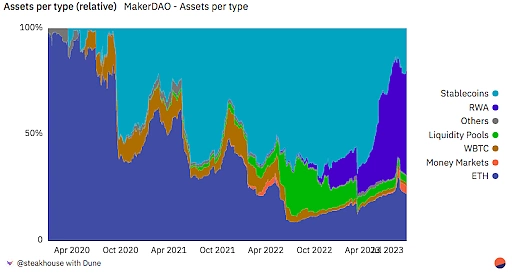

RWA/Exogenous Risk

As RWA adoption grows in the crypto ecosystem, so too do the risks associated with them, even for CDP-type stables. Maker and Frax are both leading “crypto native” stablecoins that have begun pivoting to incorporating more RWA into their accepted collateral in the name of peg stability and reserve diversification. Essentially every risk discussed above in the “Risks of Centralized, Fiat-collateralized Stablecoins” section now applies to these RWA portions of the collateral. Anytime a protocol introduces anything non-native to its blockchain, it then inherits all the risks associated with the “real world”: counterparty, custody, regulatory, etc. Blockchain code has no ability to recognize these things and, should any issues arise, they must be handled at the social layer, diminishing the “law is code” and immutability aspects of a blockchain. To make matters worse, there is very little case law for such matters in 2023, making any legal issue involving RWAs and blockchains a new, potentially messy, and almost certainly a controversial undertaking.

Risks of Algorithmic Stablecoins

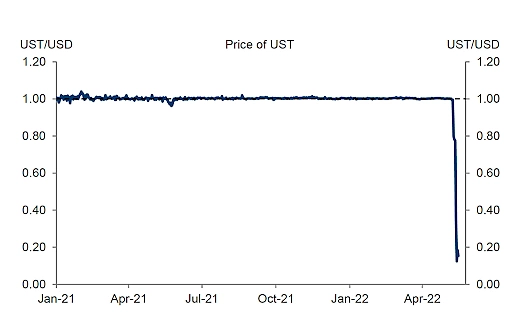

Nearly all of the aforementioned risks above also apply to algorithmic stablecoins. However, algorithmic stablecoins contain one, extremely important, risk that the others do not: endogenous collateral that is susceptible to increased reflexivity in volatile markets. Terra’s UST stablecoin is the poster child for such risk.

UST’s “Death Spiral”/Reflexive Liquidation Risk

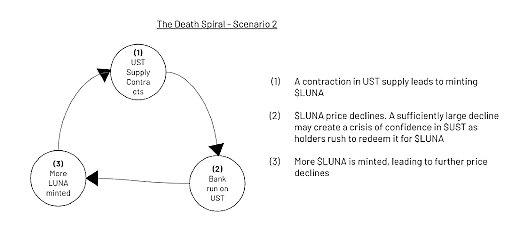

At its height, UST, Terra's stablecoin, held an impressive market capitalization of over $18.7 billion, ranking as the third-largest stablecoin globally. However, as macroeconomic challenges, including rising inflation, looming rate hikes, and a general downturn in the equity markets, emerged in early May 2022, the cryptocurrency market began to decline precipitously, including LUNA, the endogenous collateral backing UST.

LUNA's value began to crash (not uncommon in the crypto world), reducing the incentive to swap with UST, which subsequently led to the destabilization of UST's peg to the U.S. dollar. The downward momentum on UST initiated a feedback loop, often termed a "death spiral." Arbitrage traders exchanged UST for LUNA, subsequently selling it. This caused LUNA's price to plummet, requiring even more LUNA to be produced for every UST redeemed. This cycle led to a rapid increase in LUNA's supply, resulting in hyperinflation.

As Terraform Labs intervened to restore balance by adjusting UST liquidity in key pools, their efforts proved ineffective against the prevailing selling pressure. The situation was exacerbated by a mass withdrawal from the Anchor Protocol, further devaluing UST.

In response, the Luna Foundation Guard (LFG) liquidated significant BTC reserves, lending these assets to stabilize the UST peg. Despite these efforts, UST's value plummeted to $0.63. Amidst the chaos, LUNA's price experienced a sharp drop, and Terra faced insolvency concerns. Attempts to mitigate the downward spiral intensified the market sell-off, with LUNA entering a hyperinflationary state. The once-thriving Terra ecosystem witnessed dwindling confidence as all three primary liquidity pools faced disruptions, pushing LUNA's circulating supply into hyperinflation and the UST peg into further decline toward $0.

---

Disclaimer: This research report is exactly that — a research report. It is not intended to serve as financial advice, nor should you blindly assume that any of the information is accurate without confirming through your own research. Bitcoin, cryptocurrencies, and other digital assets are incredibly risky and nothing in this report should be considered an endorsement to buy or sell any asset. Never invest more than you are willing to lose and understand the risk that you are taking. Do your own research. All information in this report is for educational purposes only and should not be the basis for any investment decisions that you make.

Or check it out in the app stores

Or check it out in the app stores