What is Liquidity Efficiency in DeFi?

Liquidity efficiency means making optimal use of available capital. Liquidity efficiency is essential in DeFi as dApps require liquidity to function, and bolstered liquidity levels improve the efficiency and usability of the service provided, further drawing more users.

Key Takeaways

-

Liquidity is essential for the viable function of financial services, and increased liquidity efficiency introduces a powerful flywheel effect for DeFi.

-

DeFi faces several unique hurdles for increasing liquidity efficiency: the fragmentation and siloed nature of capital residing on different blockchains and the hard money aspect of digital assets.

-

Increased liquidity efficiency remains critical for the sustainability and future expansion of DeFi.

Recent events in the banking sector provide a tangible example of how crucial liquidity is to financial services. A lack of liquidity opens the door to systemic risk. Liquidity is the fuel for economic engines; without it, they cannot function. DeFi services mirror TradFi in this element; dApps do not work without liquidity.

DeFi must become more efficient and faces unusual challenges given the established headwinds of fragmentation and the siloed nature of liquidity on separate blockchains. Markets thrive on optimization, and introducing greater liquidity efficiency improves the efficacy of services for end users. It allows greater yield and sustainability, and the saved capital can be leveraged in other areas of DeFi, leading to an enormous flywheel effect, massively expediting the overall growth of DeFi.

The Role of Capital and Liquidity

Starting from the base layer, the importance of capital becomes overwhelmingly apparent. Layer 1s, such as Ethereum, need capital to provide platform functionality. Capital gives the token value, incentivizing miners and validators to provide computational hardware and establishing platform functionality and security.

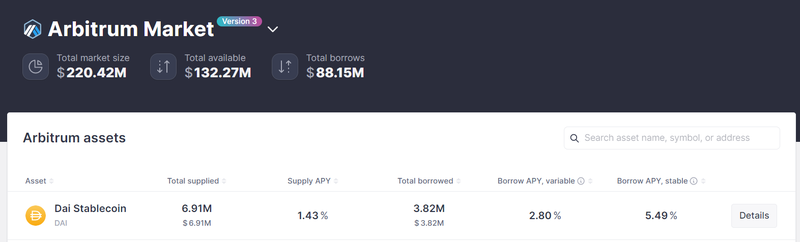

DeFi protocols cease to function without liquidity. Consider Aave, DeFi’s largest lending protocol. It has a supply side and a demand side. The supply side provides liquidity, and the demand side pays for the service with interest payments from the loans distributed to liquidity providers.

The pool's utility allows borrowers to leverage their existing assets. If the pool had no suppliers, borrowers would have no assets to access, and the pool would lose functionality. Similarly, if the utilization rate of the pool reaches 100%, suppliers can no longer withdraw assets, and borrowers cannot take loans. Again, the pool loses functionality.

The pool needs liquidity to function, and its utility improves as it attracts more capital. The capital hurdle, broadly understood as the cold-start problem, is an issue many DeFi protocols face. Liquidity enables functionality and guarantees security. Once protocols cross a liquidity threshold – typically a few million dollars – they become established and are perceived as legitimate. Investors only need to look at the prevalence of incentives to understand how important it is that protocols capture liquidity.

Greater liquidity efficiency would allow protocols to share market liquidity, enabling each viable protocol sufficient levels for functionality, widening the choice for users, driving competition, and expanding the overall use case.

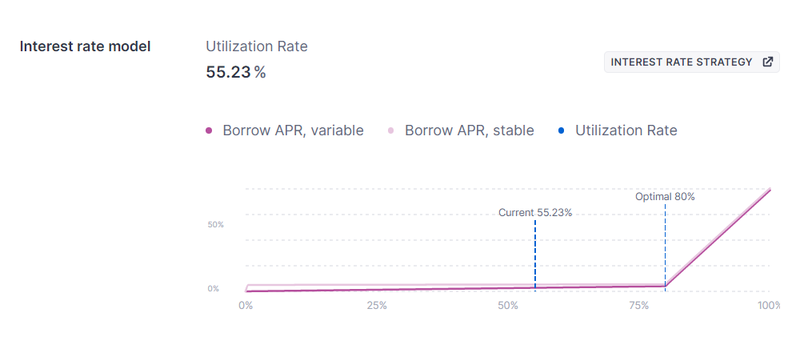

Aave employs a dynamic interest rate model to nudge market participants to be more efficient actors. When utilization rates are high, the supply APR increases naturally, encouraging users to deposit, and similarly, the borrow APR spikes, pushing users to repay borrowed funds. This financial mechanism spurs greater efficiency in capital allocation, and these mechanisms can be observed throughout DeFi encouraging market participants to act with increased efficacy.

Beyond this, liquidity efficiency improves yield for users. Almost all modern protocol business models can be broken down into three simple constituent parts: the supply side provides a service often in the form of liquidity, the demand side pays for the service, and token holders capture part of this payment in the form of financial dividends. Increased liquidity efficiency results in increased revenue for the supply side, more cost-effective service for the demand side, and better returns for token holders.

An Example of the Flywheel Effect Brought on by Better Liquidity Efficiency in DeFi

Uniswap dominates regarding decentralized exchange trading volume. Uniswap does have a first-mover advantage, but beyond this, its impressive volume results from greater efficiency. Uniswap has the largest liquidity pools with the greatest depth; therefore, traders experience the lowest slippage when utilizing these pools – the most effective use of capital.

The Flywheel: Users create LP tokens and deposit them in the pool to earn trading fees. A greater number of LP providers means better liquidity depth, and better liquidity depth means lower slippage for traders; therefore, more trades are routed through these pools. Due to more swaps being made, the pool earns more trading fees, and the increased volume of trading fees attracts more users to participate in the pool. This further increases the liquidity pool’s depth and improves the trading experience.

The Meta Shift Toward Decentralized Services

Fragmentation

DeFi’s nature poses several unique challenges to capital efficiency. Earlier reference was made to the fragmentation and the siloed nature of liquidity within DeFi. In simple terms, liquidity exists in different zones and cannot be fully optimized. The development of cross-chain solutions has been an area of contention, with the majority of exploits in crypto targeting bridges. Vitalik himself warned against bridges due to the fact they cross ‘zones of sovereignty.’

But something can be gleaned from this development. A metric investors can apply to judge the importance of a problem is how much development takes place around it. For example, scalability, or the lack of it, caused a fresh platoon of alternative Layer 1 blockchains, all touting transactions per second as their barometer for success. It also led to the Layer 2 vertical scaling race.

Referring back to fragmentation, the solution, interoperability, has similarly led to several projects being developed, with notable examples at the base layer being Polkadot and Cosmos. On the application layer, Axelar Network presents the newest player attempting to shore up the security of cross-chain transactions – even developers behind Optimism’s OP stack aimed at this problem.

Regarding liquidity efficiency, DeFi has seen the implementation of financial mechanisms for users, such as supply-driven interest rates, upgrades to the protocol level, such as Uniswap’s V3 pools, and their prevalence informs users of the issue’s importance.

Hard Money

One critical difference between TradFi and DeFi is the ‘hard money’ aspect. Fiat currency theoretically has no limit on the total supply. This has been seen during periods of financial crisis where central banks have printed money- increased the total supply to recapitalize the economy.

The idea of credit also has not reached mainstream adoption in DeFi (currently). Compared to fractional reserve banking, DeFi remains far more rigid, loans require over-collateralization, and DeFi displays traits more consistent with Austrian economics, which more broadly informs crypto compared to modern fiat currency. Without an elastic supply, it becomes even more critical to be efficient with what exists.

One of DeFi’s primary forms of collateral, Ether, has no max supply and could be a potential reproach to this line of argument. However, due to EIP-1559, which burns a portion of each gas fee, and the switch to Proof of Stake, ETH as an asset has become deflationary. Even Ethereum’s transition to Proof of Stake was motivated by capital efficiency to reduce issuance to miners. And with a decreasing supply, it compounds again the importance of making optimal use of the asset.

Lack of Centralized Participants

TradFi financial services have honed their liquidity efficiency over decades, in some cases centuries. DeFi is still in its infancy, and its open approach means it relies on the community instead of centralized actors. The core example of this is liquidity pools.

Instead of centralized market markers and order book models, DeFi primarily uses the Automated Market Maker model, which enables permissionless trading. This model has seen numerous upgrades, notably Uniswap V3 pools and TraderJoe’s Liquidity Book Model. In the original design, capital distributes evenly along the price curve despite most trading occurring in a tight range. The bulk of capital was not utilized. Thanks to these advances at the protocol level, dormant capital can now be leveraged in other locations. Other innovations to this liquidity model include the Ve(3,3), popularized by Cronje’s Solidly protocol and currently enjoying a resurgence with numerous forks.

DeFi introduced permissionless services that rely on community liquidity; this is the core offering of DeFi, financial services without centralized points of control. However, with increased decentralization comes increased operational complications. Services need and must attract liquidity. In TradFi, there are shadowy centralized figures with deep pockets acting as market makers, while DeFi relies on its user base, and given the less capitalized nature of participants, it makes effective use of available funds more imperative.

Further blows to overall liquidity levels have further accentuated the need for improved liquidity efficiency. Throughout 2022 the explosion of centralized actors such as Three Arrows, Terra, FTX, and Alameda Research thinned liquidity, the FED’s ongoing quantitative tightening draws liquidity out of the overall economy, and most recently, Jane Street and Jump Crypto announced they would be scaling back operations. All these events have skimmed liquidity from DeFi, again compounding the need for greater efficiency.

Liquidity Efficiency and Opportunity

As DeFi builds out its offerings, arbitrageurs continue to act as natural guardians closing inefficiencies, but more must be done by users and on the protocol level. The liquidity flywheel remains one of DeFi’s most significant drivers. And the composable nature of DeFi means that efficiencies spill out into other protocols benefiting a broader range of sectors within DeFi and rapidly establishing a positive feedback loop.

Liquidity efficiency improves the cost of services for users, encouraging a more extensive user base, which creates stability, leading to more users, and the flywheel activates. Improved liquidity efficiency will make DeFi more suitable for more diverse use cases, and it goes beyond increasing yield for participants; it centers on creating the conditions for DeFi to thrive as an alternative financial system.

Or check it out in the app stores

Or check it out in the app stores