Real World Assets (RWA) in crypto refers to the tokenization of tangible assets that exist in the physical world, that are brought on chain. They also include the growing issuance of capital market products on-chain, where digital securities are tokenized and offered to retail customers.

Key Takeaways

-

Decentralized finance (DeFi) yields have dried up, inching closer to traditional finance (TradFi) yields.

-

Increased tokenization of real world assets, including real estate, loans, and most recently US Treasuries, is a new source of yield in DeFi, providing opportunities for higher yield and portfolio diversification.

-

One concern around real world assets is the default risks faced by real world assets protocols due to undercollateralized loans.

The DeFi industry has boomed over the past few years, reaching the peak of $181.22 billion on 02 Dec 2021.

Source: DeFiLlama

DeFi TVL dropped drastically in 2022 and most of 2023, due to black swan events like the fall of Luna and FTX. The poor tokenomics associated with most tokens have led to inflationary pressure, causing token value to drop by more than 90%. Coupled with these issues, we can see that the DeFi yields have also decreased significantly. The days of easy DeFi yield have passed, and the industry is at a point where DeFi yields are almost on par with that of TradFi yields. Given the lower risk that the TradFi market possesses, DeFi participants have started to exit from DeFi, pivoting their capital into the TradFi market for better risk to reward.

This has sparked discussions in the DeFi industry, with market participants sourcing for higher, and more sustainable yields, as well as exploring new trends and opportunities like liquid staking. In 2023, we saw real world assets stepping up to attract the market’s attention, offering a different method to earn yield, as the name suggests, by tapping on real world assets such as loans, with interest in real world assets peaking in October at almost $6.3 billion.

In this article, other than understanding about real world assets, we will look at some of the most prominent real world assets protocols, including stUSDT, Ondo Finance, Backed Finance, MakerDAO, Creditcoin, Maple Finance, Centrifuge and Goldfinch.

What Are Real World Assets (RWA) in Crypto?

These are tangible assets that exist in the physical world. Examples of these are real estate, commodities, art, and even US Treasuries. Real world assets are a significant composition of the global financial value. The value of global real estate was $326.5 trillion in 2020 while the gold market capitalization is $12.39 trillion.

Evidently, real world assets are huge in the traditional finance industry. However, these assets are hardly tapped on in the DeFi world, beyond fiat-backed stablecoins like USDT and USDC. This brings about the possibility of inclusion of real world assets in the DeFi industry, increasing the liquidity available, and offering a novel asset class for DeFi participants to leverage on for investment yield. In addition, it should be noted that with real world assets, the investment yield could be less affected by crypto’s volatility. There has also been an increase in interest in bringing US Treasuries on-chain, offering investors a low-risk method to generate yield.

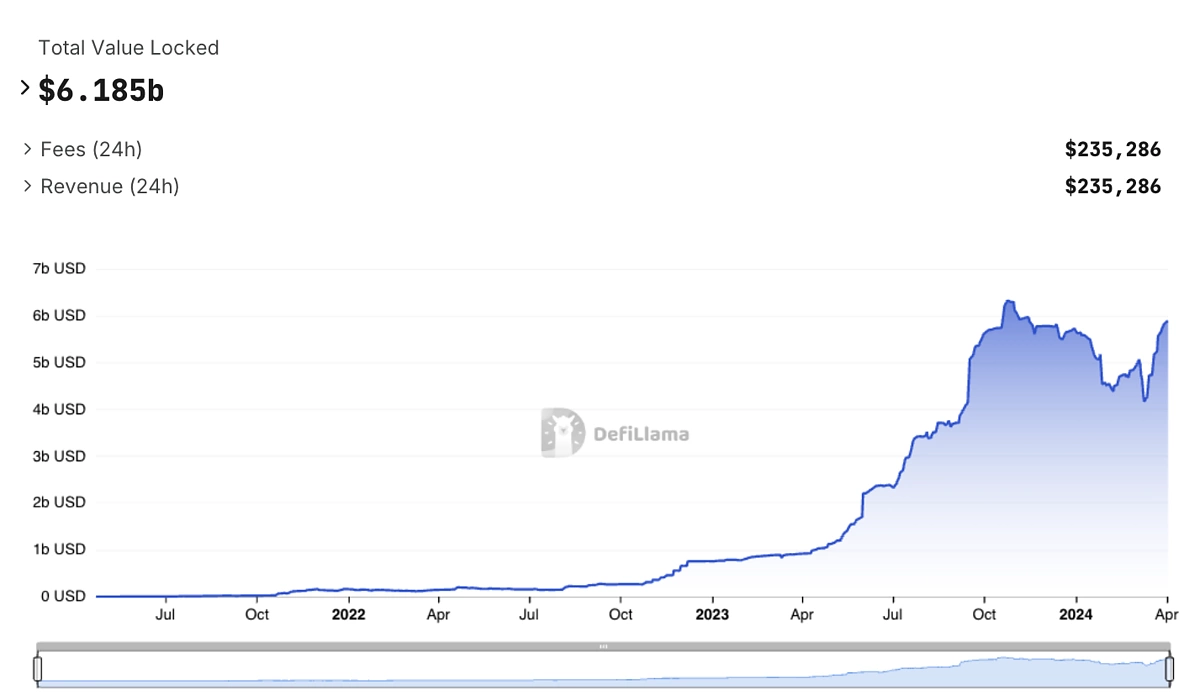

RWA is growing in the crypto space, as seen in the DefiLlama chart below, with a TVL of over $6 billion in April 2024.

Beyond bringing real-world assets on chain, there is also a growing issuance of capital market products on-chain. These include companies like Mitsui enabling asset management with digital securities, where the firm offers investments in stable operating real estate and infrastructure to retail customers. Tokenization of these digital securities is done in collaboration with LayerX and issued on a SBI and Nomura consortium-owned chain. The firm now has an estimated ¥2T in assets under management.

Beyond private chains, institutions are also looking into subnets. In April 2023, financial institutions joined Avalanche Evergreen Subnet, Spruce. These institutions will be using Spruce as a testnet to judge the benefits of on-chain execution and settlement, using DeFi applications to execute foreign exchange and interest rate swaps, with future exploration of tokenized equity and credit issuance, trading and fund management.

On-chain protocols have also started to show increased interests in integrating real world assets. A prominent example is Avalanche Foundation’s recent $50 million allocation to invest in tokenized assets created on Avalanche. With this allocated funding, it can serve as an incentive to attract builders to create real world assets on Avalanche, and thereafter continue to support the growth.

RWA in DeFi: Generating Yield Through Traditional Investments

One reason for the increase in interest around real world assets comes from DeFi protocols that generate yield through investing user assets (generally stablecoins) into traditional investments like government and corporate bonds.

stUSDT

stUSDT contributes over $1.4 billion in RWA TVL. It is the first RWA platform on the TRON network, and is designed to function as a money market fund product.

Users can stake USDT on the platform to earn 4.18% APY at time of writing, and they will receive stUSDT as the receipt token, which serves as proof of investment in real world assets, enabling holders to earn passive income, as seen in the above diagram. Meanwhile, the RWA DAO handles the investment of user assets, and stUSDT yields is reported to come from government bonds.

Ondo Finance

Ondo Finance invests into multi-billion dollar, highly liquid exchange-traded funds, enabling stablecoin holders to tap into earn yield on their assets. This works by exchanging users' stablecoins for USD, which is then used to purchase assets, and new fund tokens that reflect these investments are minted and deposited into the user's wallet. As these assets generate yield, that yield is then reinvested into more assets, and upon redemption, these fund tokens are burned and users will receive back USDC. Depending on risk level, Ondo Finance offers between 4.5% to 7.76% APY.

Recently, Ondo Finance launched Ondo USD Yield (USDY). USDY is a tokenized note which is overcollateralized by short-term US Treasuries and bank demand deposits. With USDY, Ondo Finance is enabling investors to access yield with institutional-grade structure, which confers a higher level of security.

Backed Finance

Backed Finance tokenizes a specific category of structured products that tracks publicly traded securities. The token issued is bToken, and every bToken is backed 1:1 by an equivalent security, which is held by a regulated custodian. bTokens can only be issued to KYC’d investors. However, non-KYC’d investors are still able to get access to bTokens by buying it through secondary markets, for example, through DEXs.

Backed Finance significantly lowers the existing barrier to investing in publicly traded securities. Particularly, people in emerging markets generally have difficulties accessing investment opportunities into publicly traded securities. With Backed Finance, the access to such securities is democratized.

Currently, there are a few products that are being provided by Backed Finance, with 2 categories

-

Tokenized Fixed-Income

-

bC3M: Backed GOVIES 0-6 Months Euro Investment Grade

-

bHIGH: Backed HIGH € High Yield Corp Bond

-

bIB01: Backed IB01 $ Treasury Bond 0-1yr

-

bIBTA: Backed IBTA $ Treasury Bond 1-3yr

-

Tokenized Equities

-

bNIU: Backed Niu Technologies

-

bCOIN: Backed Coinbase Global

-

bCSPX: Backed CSPX Core S&P 500

Real World Assets in DeFi: Credit Protocols and Their Tokens

Over the past few years, and in 2022 particularly, the market has seen the rise of protocols tapping on credit markets in traditional finance. This comes as no surprise given that credit is the key to businesses growing.

Businesses typically use capital to invest in research and development, grow their team and carry out marketing efforts. They can access capital through either debt financing or equity financing. Debt financing is usually preferred by teams, given that it allows them to retain control over their business while gaining access to the capital required.

The emergence of on-chain credit protocols allows for such businesses to tap into the DeFi ecosystem for capital, where the total active loan value of the top 7 private credit protocols is currently at $446 million after suffering defaults when the crypto market crashed in 2022. Based on data from rwa.xyz, the demand for private credit is largely concentrated across emerging markets, spanning industries ranging from automotive and healthcare to business financing.

Having understood what real world assets are and how on-chain credit protocols generally work, we can now dive into some of the biggest players in this particular sector.

MakerDAO

MakerDAO has been one of the most active protocols working on integrating real world assets into their operations. Recently, it was revealed that an estimated 80% of fee revenue earned by MakerDAO was generated from real world assets. With such a strong cash flow supporting its treasury, this is highly beneficial for MakerDAO given that the core product of the protocol is DAI, a decentralized overcollateralized stablecoin.

Last year, MakerDAO’s founder pushed out the plan for MakerDAO Endgame, which consists of subDAOs that manage various aspects of the protocol. As part of the future vision, the Endgame predicts that RWAs will be heavily scrutinized and regulated. As such, the team is working towards acquiring Physically Resilient RWAs that will allow the DAO to retain some level of technical soverignty over such assets. RWAs also function as a type of collateral in the Maker Protocol, which require legal entities to represent the MakerDAO in order to interact with "real world" counterparties in deals ratified by governance.

Creditcoin (CTC)

The Creditcoin protocol is designed to integrate with fintech lenders in emerging markets and connect them to DeFi investors. By recording borrower loan performance on-chain, the protocol enables trustless and transparent financial auditing for investors. The protocol’s upcoming 3.0 upgrade is promising to deliver EVM-compatible ‘universal smart contracts’ which are able to connect RWA investors across multiple chains.

There are four parties involved:

Creditcoin: A credit history protocol used for institutional auditing.

Borrowers: These are fintech lenders in emerging markets seeking to raise debt capital.

Investors: These are DeFi investors who join the Investor DAO to lend to Borrowers.

Gluwa: The protocol’s developers who propose Borrowers to Investors, perform due diligence and assist with Creditcoin integration.

This is how lending is carried out on Creditcoin:

- Gluwa sources emerging market Borrowers looking to integrate with the Creditcoin Network and raise financing, performing due diligence, negotiating terms, securing legal agreements and providing technical integration assistance.

- The Borrower integrates with the Network and records their loan performance on the Creditcoin Network using CTC.

- The Gluwa fund offers negotiated Investment Opportunities to Investors. Investors must then choose to accept or reject the Investment Opportunity, using on-chain credit performance data to help them.

- If investors allocate enough USDC to an Investment Opportunity, it is accepted and goes live following the investment deadline.

- Investment funds are then transferred and tracked on the Creditcoin Network.

"With over 3 million loan transactions recorded to-date, investors on Creditcoin can know exactly how and where their funds are being used at any time, building the trust needed to connect capital from Web3 to high-yield RWA opportunities in emerging markets."

- Tae Oh, Founder of Creditcoin

Maple Finance (MPL)

Maple Finance is an institutional capital market infrastructure, creating the platform for institutional borrowers to tap on the DeFi ecosystem for loans.

There are three parties involved:

-

Institutional borrowers: These are the participants who require loans

-

Lenders: DeFi participants who deposit capital into the pools on Maple Finance

-

Pool Delegates: Credit professionals that underwrite and manage the pools on Maple Finance.

This is how lending is carried out on Maple Finance:

-

Pool delegates source for institutional borrowers. They will conduct due diligence, underwrite and negotiate terms with the institutional borrowers. This includes Know Your Customer (KYC) and Anti-Money Laundering (AML) processes.

-

Once it has been established that these institutional borrowers are suitable for borrowing, the pool delegates will set up the pools on Maple Finance, which will be managed by them thereafter.

-

Lenders will go onto Maple Finance and identify the pools that they wish to deposit into. This will be based on their risk appetite and whether they think that the terms set out in the pools are favourable for them.

-

Once lenders have deposited capital into the pool, the institutional borrowers can now access the capital. Given that these borrowers have been whitelisted by the pool delegates, undercollateralized borrowing is made possible.

Source: Maple Finance

Goldfinch (GFI)

The protocol is focused on lending to real world businesses, and particularly, businesses within emerging markets. Goldfinch caters to a diverse range of businesses and offers attractive yields that go up to 30%, as apparent from their pools.

There are three parties involved:

-

Borrowers: These participants propose Borrower Pools to seek capital financing through Goldfinch

-

Investors: Participants that provide capital to borrowers. There are two types of investors: Backers and Liquidity Providers

-

Auditors: Participants who conduct due diligence to ensure that borrowers on boarded onto Goldfinch are not engaged in fraudulent activities.

This is how lending is carried out on Goldfinch:

-

Borrowers first undergo an audit by auditors to determine that they are eligible to loan.

-

Once approved, borrowers can create borrow pools and determine the credit terms, which includes metrics such as interest rate, limit, payment frequency, term and late fee.

-

Investors can now come in to supply capital.

-

Backers supply capital directly to the borrower pools and are the first loss capital. Hence, they receive a higher return.

-

Liquidity providers supply capital to Goldfinch, which is then allocated across all borrower pools.

Source: Goldfinch Finance

Centrifuge (CFG)

The protocols mentioned above have all been a good example of incorporation of real world assets into the DeFi ecosystem. However, they are all focused on the credit aspect. To bring more colours into the on-chain credit ecosystem, Centrifuge comes around to allow for more forms of real world assets to be brought onto the ecosystem, and has a slightly different mechanism by incorporating Non-Fungible Tokens (NFTs).

There are two parties involved:

-

Asset Originators: These are the borrowers that tokenize their real world assets into NFTs

-

Investors: These are the lenders.

Centrifuge’s decentralized application (dApp) is known as Tinlake, serving as a marketplace and investment dApp.

This is how lending is carried out on Tinlake:

-

An asset originator bridges a real world asset using Tinlake. This asset is converted into an NFT, which includes relevant legal documentation.

-

Asset originators can now create asset pools using the tokenized real world asset NFT as underlying collateral.

-

Upon pool creation, two tokens are created: DROP tokens and TIN tokens.

-

Investors can decide which pool to provide capital into based on their individual risk profile, buying either DROP or TIN tokens.

-

DROP token holders have a guaranteed return, determined by a fee function that has a fixed interest per pool, compounded every second.

-

TIN token holders, on the other hand, do not have a guaranteed return. They receive a variable yield that is based on the investment returns from the pool, which could be higher than the returns from holding DROP tokens.

-

TIN token holders borne a higher risk as they take the first loss in the event a borrower defaults.

Source: Centrifuge

Advantages of Credit Market Protocols

There are a variety of advantages brought about by credit market protocols. There are two angles to view this.

1. DeFi Participants

As of this current point, the yields offered by credit protocols are higher than that of most DeFi protocols. The APY provided by each of the protocols are as follows:

-

Maple Finance: 8.31%

-

TrueFi: 2.08%

-

Centrifuge: 9.31%

-

Goldfinch: 8.31%

In addition, DeFi participants will be able to diversify their portfolio, given that institutional borrowers that run real world businesses are less correlated to that of the crypto market.

2. Emerging Markets

It is typically difficult for businesses in emerging markets to receive undercollateralized loans. This is because of the higher requirements that have been set in stone in the traditional markets. Such regulations make it extremely difficult for small businesses to scale, given that they are unable to access capital and even if they were able to, it would come at a huge cost to them, undermining their runway to scale.

The DeFi ecosystem presents a new source of loans, and increases their capital efficiency given that undercollateralized lending is made possible. This is also a benefit that results from the removal of middlemen and utilization of smart contracts for certain operations.

In addition, by borrowing on-chain, these businesses are building their on-chain credit profile. By paying their loans on time, they will be better positioned to receive more loans in the future, and these loans can even be of a higher quantum.

Disadvantages of Credit Market Protocols

The greatest risk that exists would definitely be the default risk posed by the borrowers. Given that these are undercollateralized loans, the lender will not be able to receive their full capital in the event of default. This has been an ongoing problem, apparent from some protocols:

-

Maple Finance: $69.3 million

-

TrueFi: $4.4 million

-

Centrifuge: $2.6 million

It should also be noted that despite the protocols reducing the amount of crypto volatility faced by lenders because of the usage of stablecoins, it is still subjected to the bigger fallouts in the industry. This is very evident from Maple Finance’s case where close to half of its default came after the FTX fallout.

Other than the impact on lenders, protocols could also suffer from bad debt, undermining the protocol’s longevity.

The other inherent flaw with the current credit protocols would be that of human bias. The KYC and AML process, along with the whitelisting of borrowers, are being determined by humans.

Real World Assets Protocols’ Token Performance

So how have the credit protocols performed? All the native tokens have underperformed Ethereum by more than 20%. The following table shows the drop in price since their all-time highs:

| Protocol | Change in Price Since ATH |

| Ethereum (ETH) | -32.2% |

| Maple Finance (MPL) | -66.8% |

| Goldfinch (GFI) | -85.6% |

| Centrifuge (CFG) | -54.4% |

Despite the adoption of credit protocols, with 1,847 loans issued, total loan value of $4,440,662,580 and active loan value of $608,827,760, the protocols have yet to perform well on the token front as of time of writing.

Conclusion

Real world assets is an interesting vertical with lots of potential, given how huge the market is in traditional finance. We have seen the space being occupied by multiple credit protocols, each with a twist on how they run the protocols.

However, it should be noted that despite the advantages that it brings about such as diversification of portfolio and higher yields, the risk of default is an area that has yet to be addressed successfully. The only exception would be Goldfinch, which has not faced a single default since starting.

In addition to the credit market, there are also other real world aspects that have been gaining market interest. An example of which would be the tokenization of real world assets such as real estate or art. With the digitalization of such assets on-chain, fractionalization of the asset is made possible, allowing people to have partial ownership.

This will be an exciting space to watch, given the rapid developments done by the protocols and we can look forward to more adoption from the market.

This article is for educational purposes and should not be taken as investment advice. Always do your own research before investing in any cryptocurrencies or protocols.

Subscribe to the CoinGecko Daily Newsletter!

CJ is a business graduate that has been involved in crypto for 4 years and specializes in DeFi protocols. He is also interested in TradFi becoming DeFi, and has written for ByBit, SwitcheoLabs, and others. Follow the author on Twitter @fishmarketacad

Or check it out in the app stores

Or check it out in the app stores