What Is Pendle Finance?

Pendle is a Decentralized Finance (DeFi) protocol that enables the separation and subsequent trading of yield from yield-bearing assets. In more recent times it has also been used by users as a platform for farming points and airdrops.

Key Takeaways

-

Pendle is a yield-management protocol which allows traders to tokenize and trade the yield from yield-bearing assets. It is DeFi’s answer to TradFi’s interest rate derivative market.

-

The protocol consists of three main features – yield tokenization, yield trading, and the PENDLE token.

-

Users typically use Pendle for three main strategies - locking in a fixed yield, longing yield, or shorting yield from yield-bearing assets.

Why Is Pendle Unique?

With the boom of DeFi in 2020, yield-farming has been one of the prime activities for DeFi traders looking for more passive ways to earn income. To yield-farm, a trader would provide or lock up some capital into a DeFi protocol, in order to earn a promised return, typically measured in Annual Percentage Yield (APY). This is analogous to fixed deposits or purchasing a bond in traditional finance (TradFi). This demand for yield-farming led to projects building platforms to better enable traders to capture such opportunities. Early yield-farming protocols such as Yearn focused on yield aggregation, but Pendle represents the next innovation in this space.

Pendle enables yield-farmers to have more minute and capital-efficient management of their yield-farming opportunities by allowing traders to tokenize and trade yield from yield-bearing assets. This is crucial as DeFi yields tend to fluctuate from time-to-time, depending on many different factors, such as future capital inflows, and the existence of an airdrop down the line. Selling his / her yield when the APY is high may allow a trader to lock in gains ahead of time, and also unlock some level of liquidity for the next opportunity. Conversely, another trader who may want to speculate on the yield of a certain protocol but does not want to commit significant amounts of capital for staking can just purchase the yield tokens from the first trader, or use Pendle to separate the yield of his / her asset from the principal, and then sell the principal immediately.

While it initially launched in mid-2021 with little fanfare, activity on Pendle was supercharged at the beginning of 2024 with the introduction of Eigenlayer’s restaking mechanism and the ensuing “Points meta” from liquid restaking protocols (LRTs) such as Ether.fi, Renzo and Kelp. These LRTs gave out “points” in proportion to capital staked over a length of time, with the promise of a token airdrop proportional to the amount of points a user has. As these “points” also counted as a portion of the yield, Pendle’s yield tokens became one of the easiest ways to acquire these points, while also allowing traders to speculate on the actual value of these token airdrops.

How Does Pendle Work?

Pendle delivers permissionless yield management, and the protocol has three core features.

1. Yield Tokenization

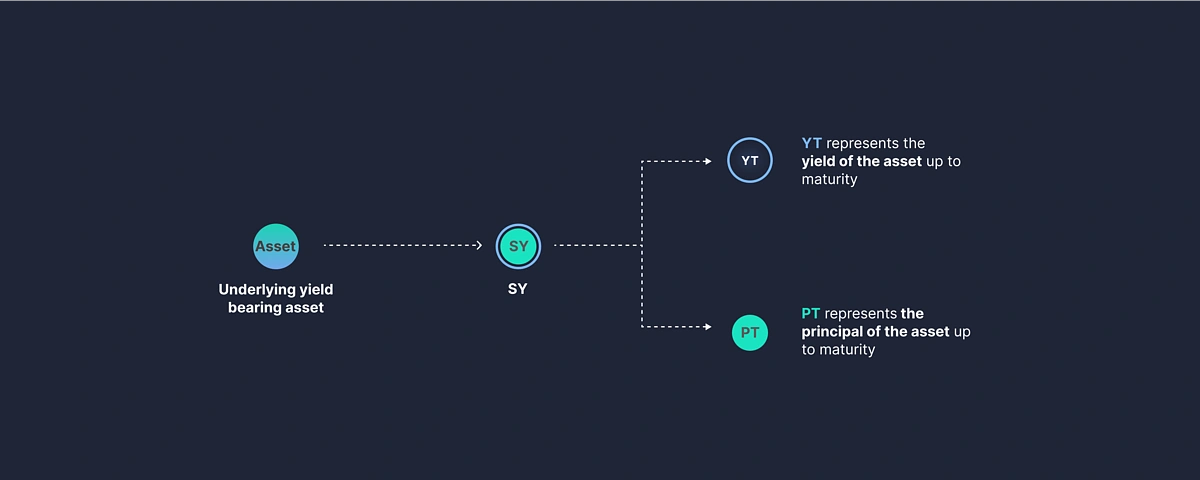

Pendle uses the SY (Standardized Yield) EIP-5115 token standard for wrapping yield-bearing assets. Principal Tokens (PT) and Yield Tokens (YT), representing the principal and the yield of the asset, can then be minted from SY tokens.

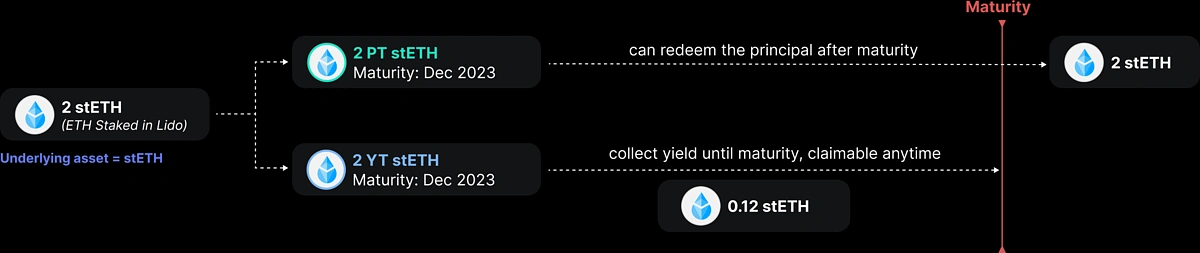

Using Lido’s liquid staked-ETH as an example, staking ETH with Lido results in the trader receiving stETH, which represents the amount of ETH the trader staked in Lido, and also accrues staking rewards over time.

The trader can then deposit his / her wstETH (the ERC-20 version of stETH) into Pendle, which wraps it into SY-wstETH tokens. From there, the protocol will then mint the corresponding PT-wstETH and YT-wstETH tokens. PT-stETH is the principal, in this case the initial amount of staked Ether, and YT-stETH is the yield, i.e. the staking rewards from Lido. For each of these SY, there is also a fixed maturity period.

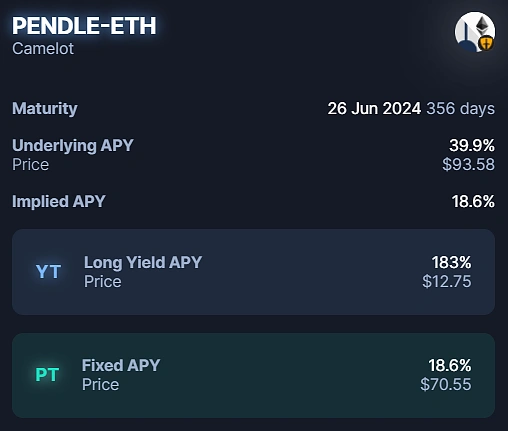

Understanding the different APYs featured Pendle is essential before users begin trading YTs and PT tokens.

-

Maturity is the time period until a PT can be redeemed for the underlying asset and the window within which the YT produces yield.

-

Underlying APY shows the seven-day moving average APR of the core asset (in the above example Ethereum staking rewards from Lido)

-

Implied APY is what the market thinks the future APY of the core asset will be

-

Long Yield APY is the reward for buying and holding YT assuming the asset’s base yield remains constant

-

Fixed APY is a set and guaranteed APY available for users who want to hold a PT until maturity.

With PT and YT tokens, the user can then trade these on the Pendle AMM (more on this later), but for now we examine what happens to these tokens at maturity.

A user holding both the PT and YT tokens can redeem the underlying asset at any time for the underlying asset. A user holding only the PT-wstETH can redeem it for the underlying asset upon maturity without the YT component. Finally a trader holding only YT-wstETH collects all the staking rewards (generated yield) until maturity. However upon maturity, the value of the YT token goes to zero, as it no longer accrues yield.

2. Yield Trading

Effective trading of PTs and YTs requires a marketplace, and the Pendle AMM (Automated Market Maker) rests at the heart of the entire ecosystem. The underlying mechanism of Pendle involves traders making bets on the yield, i.e. YT tokens of yield-bearing assets.

Traders who buy YT go long on yield. They bet the yield (Underlying APY) will trade above the Implied APY – a market-driven price on the future APY of the asset. In simple terms, if the yield maintains or increases, they win. For example if users want to go long on wstETH yield, they can buy wstETH Yield Tokens (YT-wstETH) on Pendle. As long as the yield produced by these yield tokens outweighs the purchase cost, the trade is a winner.

Traders can also sell their PT prior to maturity to recoup the principal from their yield-farming strategy. Pendle pairs PT tokens with SYs and leverages flash swaps to enable YT trades through the same pool, meaning all trades for a particular asset route through a single liquidity pool. Note that PT tokens will always trade at a discount to the underlying asset as they do not include the yield component, so on the other side of the trade buyers of PT can accumulate the underlying asset at a discount if they are willing to hold to maturity.

Users who are just using Pendle to farm airdrops and do not intend to participate in the trading of YT and PT can also just act as liquidity providers in the Pendle AMM pools, earning some additional LP-fees

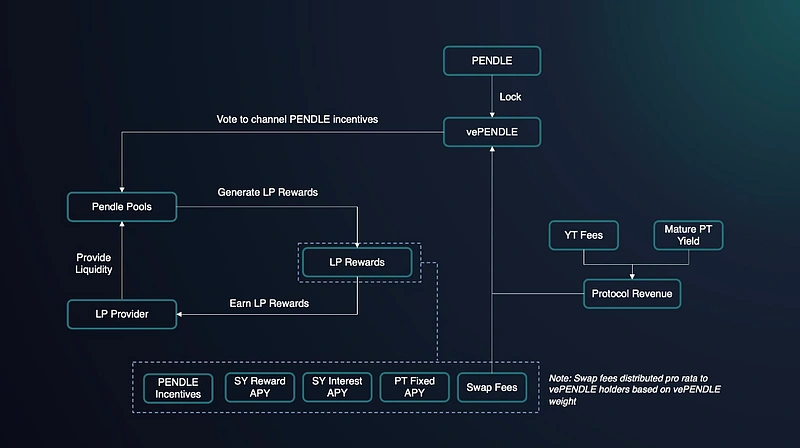

3. The PENDLE token and vePENDLE

The final piece of the Pendle puzzle is its own token, PENDLE, and a vote escrowed token: vePENDLE. PENDLE serves as an incentive token to juice the returns on Pendle pools, but by staking PENDLE, users obtain vePENDLE which gives them governance rights, allowing them to channel PENDLE incentives on the platform. vePENDLE holders also enjoy boosted yields and share in protocol revenue. A later section will discuss PENDLE and vePENDLE in more detail.

Pendle Use Case and Strategies

Here are some core use cases of Pendle:

Locking in a Fixed Yield

Users can buy a PT, hold it until maturity, and redeem the underlying asset. In this case, users lock in a fixed yield at the point of purchase.

Ideally, users want to purchase a PT when the Implied APY exceeds the Underlying APY. In this scenario, the market prices the asset assuming an increased yield. Users need to work out what they think the average yield of the asset will be and compare it against the market price.

An example: Economic activity on the Ethereum network rises (think memecoin season), leading to additional execution layer rewards for stakers. In this situation, the Implied APY may rise. If a user thinks the good times will not last, they could choose to lock in a higher Implied APY, and if they hold the asset until maturity, they will receive this Implied APY for the entire duration.

GLP is an index of assets, and the GLP pool on GMX is the counterparty to traders. More traders getting liquidated means more profit for GLP stakers. In this example, the Underlying APY is 10.5%, and the Implied APY is 14.7%. The market predicts that the GLP yield will go up, and users can bet against this consensus.

Before jumping into the trade, users should ask themselves what they think the future yield of GLP will be. If they believe the Underlying APY will rise, it is probably not a good time to lock in a fixed rate. But it would be a great time to lock in a fixed rate if they think it will remain steady or decrease.

Longing Yield

Pendle allows users to go long on yield – to bet that generated yield will either sustain or increase. To do this, users purchase YT.

Again the success of the trade boils down to the relationship between the Implied APY and the Underlying APY. Underlying APY above Implied APY is the ideal scenario for longing yield.

In the above example, a PENDLE-ETH LP token, the Underlying APY rests decently above the Implied APY – theoretically, the perfect setup for longing yield. But users again need to ask themselves if they believe the Underlying APY will sustain. Considering that PENDLE has recently received plenty of attention, this may be a short-term spike that does not persist.

But if users believe this APY will last or even increase, it would be an excellent time to be long on yield. The profitability of a long yield trade can be calculated by future yield minus YT cost.

Shorting Yield

Users can also hypothetically short yield on Pendle. Although locking in a fixed rate means users fade yield, there is a more direct method to short yield on Pendle:

Users mint an SY. Sell the YT component, wait for it to drop, and then purchase it back, combining the PT and YT to redeem the asset.

PENDLE Token and vePENDLE Explained

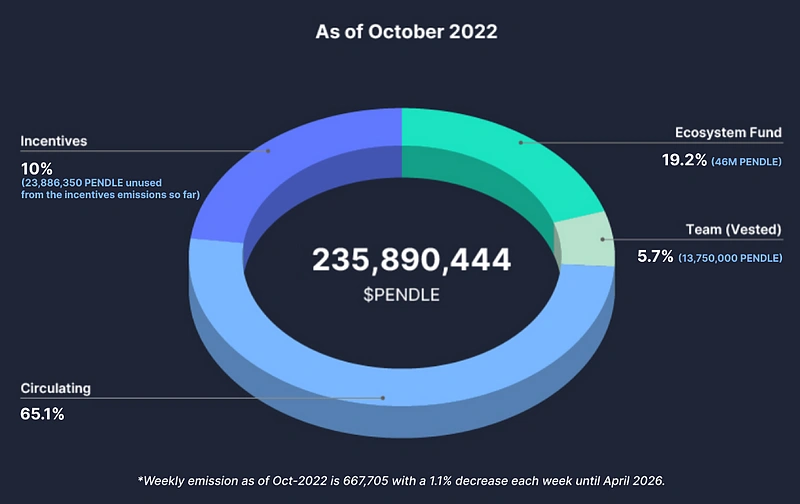

Pendle has a total supply of 281,527,448 tokens. The team mainly uses it to incentivize activity on the protocol, distributing tokens to users who utilize the protocol. Pendle has aggressively incentivized liquidity provision on the protocol by distributing PENDLE over recent months. As of October 2022, weekly PENDLE emissions totaled 667,705, declining by 1.1% each week until April 2026.

Team tokens have fully vested, and the whitepaper details that the allowed terminal inflation rate for the PENDLE total supply will be 2%.

To utilize PENDLE in governance activities, Pendle opted for the vote escrowed token model with vePENDLE. vePENDLE provides holders to the following benefits:

-

Vote to channel PENDLE incentives into a pool

-

Vote to receive Voter’s APY (80% of the swap fees of the voted pool)

-

Receive base APY

-

Boost LP rewards (up to 250%)

vePENDLE has a variable lock rate (up to two years) with a decay function encouraging users to relock their PENDLE for maximum benefits.

The generous incentives offered by Pendle have led to more than two thirds of the circulating supply being locked. The offerings include 3% of all yield accrued by YTs, 80% of the swap fees generated from the pools voted for, and up to 250% additional yield on LP positions.

Where to Buy and Trade PENDLE

Since the inception of the protocol, PENDLE is now widely listed and traded across most major centralized exchanges (CEX) such as Binance, Coinbase, OKX and Bybit. As the token is deployed across multiple chains – Ethereum mainnet, Arbitrum, Optimism, Base, BSC and Sonic, decentralized exchange (DEX) options are also available on each chain, with Arbitrum having the most liquidity.

Risks and Considerations

As Pendle’s main function is to facilitate the tokenization and trading of yield, the main risk is related to Pendle’s smart contracts that perform key functions such as wrapping / unwrapping the underlying assets into and out of SY, the minting and burning of PT and YT tokens from SY, the claiming of yield for YT holders, and the Pendle AMM trading pools. Pendle’s entire code base is open source, and the smart contracts have been audited by Ackee, Dedaub, Dingbats, and some of the top wardens from Code4rena.

The Pendle team has taken great pains to simplify the trading process, using the well-established AMM pool model with concentrated liquidity, auto-routing, and a dynamic curve, which effectively eliminates impermanent loss. Finally, the vote-escrow governance model introduces certain risk angles, mainly if malicious actors are able to amass a large amount of voting power.

Otherwise, the main risk for traders is actually on the underlying yield-bearing asset itself, which may be volatile or be impacted by significant price fluctuations. Hence it’s important to note that Pendle is not a protocol where users can just “set and forget”. Moreover, as SY assets have maturity dates, users still need to check in from time-to-time to migrate their assets to a new pool if they want them to continue to be productive.

Latest Updates and Roadmap

While Pendle’s TVL has definitely fallen off since the heydays of the first half of 2024, the team has continued to ship updates for its users. The protocol grew ~20x TVL in 2024, with 400% user growth. It has also now been deployed across 8 chains, taking advantage of the broader EVM ecosystem to expand its reach. In 2024 the protocol deployed nearly 200 pools.

At the start of 2025, TN, the Co-founder of Pendle, outlined the project’s immediate future plans in a Medium post. The strategy hinged on three main pillars:

Improvements to Pendle v2

While the entire codebase of Pendle is open source, the team is still mainly responsible for deploying new pools on to Pendle. The team will be shipping UI improvements to allow all teams to create their own yield markets. Other improvements include dynamic fee rebalancing, and improvements to vePendle.

Citadels

Citadels are initiatives which aim to expand the range of yield bearing assets and opportunities supported on Pendle. These include expanding beyond the EVM ecosystem to other non-EVM chains, such as Solana, Hyperliquid, and TON. The team is also taking aim at TradFi, looking to create a KYC-ed product for regulated institutions, as well as products compliant with Shariah principles.

Boros

Finally Boros is focused on expanding the range of yield-optimization opportunities supported on Pendle by introducing a yield perpetual product, similar to interest rate futures in TradFi. This will allow Pendle to support yield products beyond generic DeFi yield-bearing assets, potentially removing the need for an underlying asset in the first place. The first product that Boros will be focusing on are funding rates on perpetual exchanges, allowing users to hedge funding rates at scale.

Final Thoughts

The most successful DeFi protocols serve a simple and well-understood use case, and while Pendle and yield tokenization may seem like more advanced concepts, the project team has done a good job in simplifying down the key concepts to deliver a less daunting experience for users.

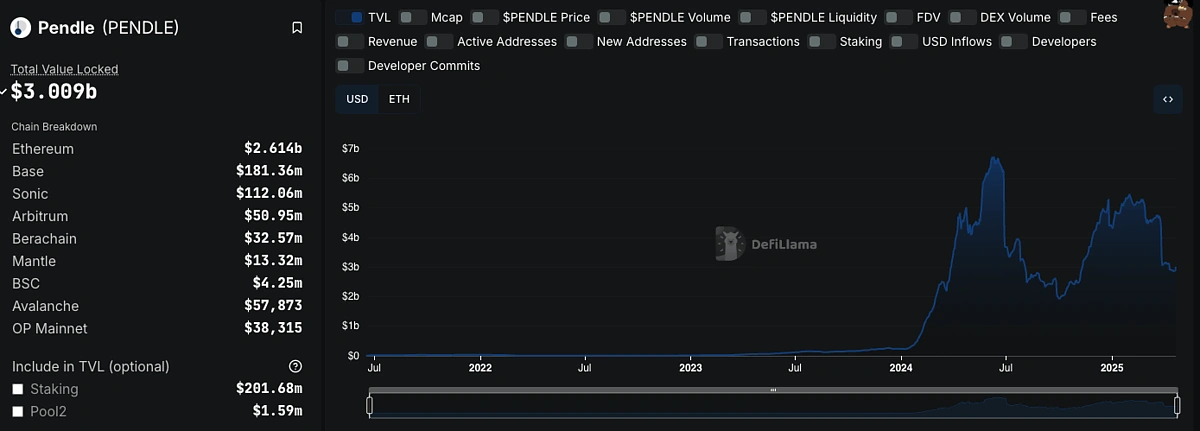

While it didn’t have the fastest start, the protocol has found product market fit (PMF) for yield-farming enthusiasts. With >$3 billion in TVL and >50% market share of the yield-management DeFi segment, Pendle is now viewed as a key source of liquidity for up-and-coming chains and DeFi protocols.

TradFi’s interest rate derivatives market has a notional value exceeding $400 trillion, and after achieving initial PMF, the Pendle team now has the opportunity to stretch its wings, and attempt to grasp greater opportunities beyond yield-farming. Its sophistication could attract a new set of users – other DeFi projects, and even TradFi institutions, who are hungry for more DeFi projects that can meet their sophisticated needs.

This article is only for informational purposes and should not be taken as financial or investment advice. Always do your own research before interacting with any protocols.

An earlier version of this article was written by Kofi J.

Or check it out in the app stores

Or check it out in the app stores