What are veTokens?

Vote Escrowed tokens (veTokens) are tokens that have been willingly locked for a period of time by a token holder in exchange for the right to participate in the governance of a protocol. Typically these tokens are non-transferable and often entail additional benefits alongside governance rights.

Key Takeaways

-

veTokenomics involve users voluntarily locking their tokens in exchange for governance rights and a share of protocol revenue

-

The purpose of veTokens is to better align users and protocols through long-term decision making

-

Each vote escrowed token should be considered individually on a protocol-by-protocol basis

The veToken model represents an approach to solving several issues at once, and this article dives into the idea behind the concept of vote escrowed tokens, touching on several of the most famous examples.

veTokens Models and Tokenomics

Vote Escrowed tokens (veTokens) aim to solve two core issues: liquidity and engagement. Almost all economic models in crypto aim at these two principles. Protocols want to attract deep liquidity, they want to attract permanent or ‘sticky liquidity,’ and they want token holders aligned with the protocol’s core mission.

Protocols have discovered they can easily pull in users for short periods through less sustainable programs such as liquidity mining. However, turning a user into sticky liquidity has proven much more challenging. And that is where veTokens come in, where VeTokenomics aim to turn a user into a long-term participant.

Simplified Example of veTokenomics

In its most basic format, veTokenomics function as in the above diagram. But crypto investors remain notoriously self-interested creatures, and simple governance rights often do not constitute a good enough incentive to lock up tokens. Therefore the typical model looks more like the diagram below.

Users lock their tokens and, in exchange, gain voting rights and a percentage of protocol fees. More broadly, protocol revenue sharing has become a core value accrual mechanism for tokens deployed over the last year. Investors no longer want governance tokens with no economic incentive, which has contributed to the collapse of value in DeFi 1.0 tokens. A final constituent of the veToken model is boosted yields.

User A locks tokens and receives veTokens in return. veTokens allow the user to participate in governance, earn a percentage of protocol fees, and earn increased rewards within the protocol. A key point, more often than not, veTokens are non-transferable and cannot be sold. Note that some variations, including NFTs within Solidly forks, will be discussed later.

Why veTokens? The Two Core Issues – Liquidity and Engagement

Liquidity and engagement. This model aims to create active participants within a given ecosystem aligned with the protocol’s long-term success. A user who locks their tokens – lockup periods can be up to four years long – makes an economic commitment to the protocol. Locking tokens for long periods means the user votes with their dollars that the protocol will still exist and function at the redemption date. The protocol’s success then becomes integrated with the user’s interests; they have skin in the game and are personally invested. The mechanism turns mercenary capital into protocol supporters – in theory, at least.

User Perspective

The user locks their tokens, allowing them to earn a percentage of protocol fees and boosted yields. A good mental framework for the user when approaching veTokenomics is to view the locked tokens as an investment for future profits.

Curve Finance offers yield boosts up to 2.5X. Therefore, it makes financial sense for a participant with significant holdings on Curve to hold veCRV. Similarly, the clones of Solidly direct the bulk, if not all, of the trading fees to token lockers alongside bribes associated with the pools, again meaning that it is in the interest of users to lock tokens to unlock the higher earning potential of these platforms.

Protocol Perspective

If only users with locked tokens can participate in governance, the pendulum naturally shifts towards a more long-term outlook when considering governance proposals. Users are more likely to consider the long-tail effects of decisions.

A lower circulating supply also allows for more explosive price discovery. Token price reigns supreme in crypto, and anything protocols can do to allow for better price action significantly benefits them – there are few things as universally accepted as positive as ‘number goes up.’ Also, protocols successful in encouraging a large percentage of users to lock their tokens benefit from bolstered liquidity and price stability.

Token emissions primarily go to users holding an escrowed token version, enforcing more responsible profit-taking. In the liquidity mining example, users arrive, soak up as many tokens as possible, then dump them on the market before moving to the next farm. In the veToken model, users who rapidly dump all their emissions put sell pressure on their own bags. This, however, has been a recurring issue, especially in ve(3,3) models; hence all the forks proposing minor adjustments to the economic model first introduced by Cronje with Solidly.

Source: https://curve.fi/#/ethereum/swap

The King of veTokenomics: Curve Finance

Curve Finance pioneered the vote escrow model, and it is impossible to discuss veTokenomics without mentioning the stablecoin giant. Curve grew into a liquidity titan by taking the AMM (Automated Market Maker) model and pairing assets that behaved similarly (stablecoins). If users want to swap stablecoins with low slippage, there is no better location than Curve.

Curve introduced the base formula for the veTokenomics model. Curve’s implementation of this strategy became so successful because of the unique financial incentives attached to CurveDAO membership. Holders veCRV decided on the distribution of CRV tokens to liquidity pools.

Source: https://resources.curve.fi/crv-token/understanding-crv

The above graphic highlights the value proposition of holding veCRV. The short summary is that if users actively engage and provide liquidity on Curve, they do themselves a disservice by not holding any veCRV. Users curious about the meaning of ‘Gauge’ will likely be more familiar with their informal name, ‘Bribes’- the method the Curve protocol uses to decide on the distribution of CRV emissions.

Only wallets holding veCRV can participate in this decision process. Curve also features a decay element meaning that the total veCRV held by a user decreases linearly, encouraging constant lockups for maximum yields – hence why the locked tokens should be viewed as an investment for future profit.

The key takeaway from Curve is the introduction of bribing – the ability of veToken holders to direct protocol emissions.

A Brief Word on the Curve Wars

veCRV holders decide on the pools that receive CRV emissions; therefore, large veCRV holders have a disproportionately large say in reward distribution. This led yield aggregators to stockpile vast amounts of veCRV tokens to ensure their pools received the greatest percentage of CRV emissions. Protocols begin to fight over veCRV dominance.

veCRV dominance became very attractive because it powered deep liquidity for protocols and allowed them to incentivize without inflating their native token. For investors, it came down to yield and who could provide the most.

Somewhat ironically, users leveraging these yield aggregators forfeited their governance rights. Enormous players emerged: Yearn Finance, Convex, and StakeDAO, all fighting to obtain the most significant share of veCRV to max out APYs.

Despite the vision behind veTokenomics to encourage thoughtful governance decision-making, users quickly abdicated their voting rights in favor of boosted yields – recurring theme observable throughout DeFi.

Enter ve(3,3): Solidly and Forks

Source: https://solidly.exchange/

The following significant change to the veTokenomics model came from Cronje and Soldily. At this point, the model gets slightly more complex.

Basic Solidly Mechanics

-

Users provide liquidity and receive SOLID

-

Users can lock SOLID in exchange for veSOLID (an NFT)

-

NFT holders can vote on pools

-

These votes decide on token emissions of SOLID

-

Voters get bribes and swap fees from the pools they vote on

-

The rebase model ensures that early lockers of SOLID do not get diluted (token emissions mean that over time lockers will own less of the total supply)

-

Any protocol can bribe these liquidity layers encouraging deeper liquidity

How Did Solidly Change the Liquidity Model?

The ve(3,3) model introduced by Cronje introduced active emissions management, meaning that instead of the centralized direction of liquidity incentives, users themselves directed emissions.

This idea comes from Curve, but whereas Curve directs 50% of trading fees to LP providers, Solidly and the subsequent models direct 100% of trading fees to veToken holders.

Solidly hard-built bribing into the DEX, and the great innovation of ve(3,3) protocols is their ability to act as a liquidity layer for ecosystems allowing smaller protocols to overcome the cold start problem via bribing. It enables protocols to attract liquidity at a more cost-efficient basis without inflating their native token.

The ideal underpinning flywheel effect for the ve(3,3) model conceptually is that increased liquidity leads to less slippage, increasing trading volume, meaning more fees, and, therefore, higher emissions, looping all the way back to more liquidity.

The key takeaway from Solidly is the active liquidity element. All trading fees go to the voters, and veToken holders only receive rewards from the pools they vote for. This financial incentive encourages people to vote for the pools generating the most trading volume. Thereby directing the bulk of protocol emissions to the most active pools.

The (3,3) part of Solidly’s ve(3,3) model comes from Olympus DAO and the game theory behind the protocol. In Solidly, it refers to the rebasing method that ensures early lockers are not diluted.

Source: https://defillama.com/forks/Solidly

Solidly Forks

Source: https://defillama.com/forks/Solidly

Solidly offered a tremendous step forward to optimize and align token holders and liquidity providers; however, it rapidly fell apart for several reasons. The lockup period (four years) is a lifetime in DeFi. A bug allowed people to vote, claim bribes, and then change their vote after the fact. Emissions in the initial weeks were enormous, disappearing practically overnight as investors pulled liquidity and the protocol died.

Most iterations of Solidly have focused on changing the token emissions schedule to make it more sustainable and predictable. They have reduced the lockup period or made it more flexible. Another key vector of innovation has been the NFTs which can be traded on the secondary market and open up the potential for merging, transferring, and splitting – a key innovator in this space has been Thena Finance. Other notable forks of Solidly include Velodrome, Chronos, Equalizer, and SolidLizard.

Whether a dominant project emerges remains to be seen. Most Solidly forks follow a consistent pattern where early high emissions encourage users to lock tokens. Once users have ROIed on their initial token lock, rampant dumping kills the value of the platform token. And nobody wants to buy a token with no upside potential.

An excellent metric for innovation within DeFi is the number of times a protocol gets forked. And by this metric, Andre’s creation Solidly permanently stamped its mark within DeFi.

The question moving forwards for ve(3,3) protocols is whether a protocol can retain liquidity by relying solely on trading fees instead of leaning on token emissions to entice users.

ve(3,3) Playbook: An Objective Viewpoint

The ve(3,3) model rewards early lockers given the rebase method that prevents dilution. Those who lock tokens promptly enjoy the early incentive yields and typically price appreciation in the native token. Users typically lock their tokens for the longest period and keep relocking them to ensure maximal yields. Hence the initial lock can be perceived as lost – a sunk investment to increase yield payout. Then the (3,3) game plays out. However, if the protocol token loses value at this stage, the ecosystem can quickly collapse as investors pull their liquidity.

A Note on Time Duration Risk

Duration risk comes from TradFi markets, specifically concerning bonds. Interest rates affect bond values; this sensitivity is called time duration risk. This topic has received attention recently, with many banks suffering heavy unrealized losses due to large amounts of long-duration bonds held on their balance sheets. Soaring interest rates have decimated the value of long-dated bonds.

Time duration risk presents the greatest danger to investors locking tokens for extended periods. And crypto has seen numerous examples of this risk-type burning investors.

GBTC Trade – The Widow Maker

The GBTC arbitrage trade undertaken by Three Arrows Capital provides an excellent example. In simple terms, 3AC leveraged its status as an accredited investor to purchase Bitcoin, provide it to GBTC to create shares, and then pocket the difference. At the time, GBTC traded at a premium because it was the only way to gain straightforward tax-advantaged exposure to Bitcoin without custody or regulatory headaches for large investors.

Where is the time duration risk? GBTC shares were locked for six months. And this six-month window marked the end of 3AC alongside the Luna fiasco. When the premium flipped to a discount, 3AC, who were incredibly leveraged in this trade, got blown up in remarkable fashion dragging the market along with them.

Time-Duration Risk Decreases as Crypto Matures

As crypto as an asset class matures, the time-duration risk present in the space more broadly decreases. However, investors still need to decide individually on each token they lock up.

The veToken model has become widely popular given its ability to lock in liquidity, enforce price stability, and encourage long-term loyalty to the protocol. Moving away from bribes and the ve(3,3) model DeFi presents plenty of examples of more simplistic veTokenomics, such as Frax and Pendle.

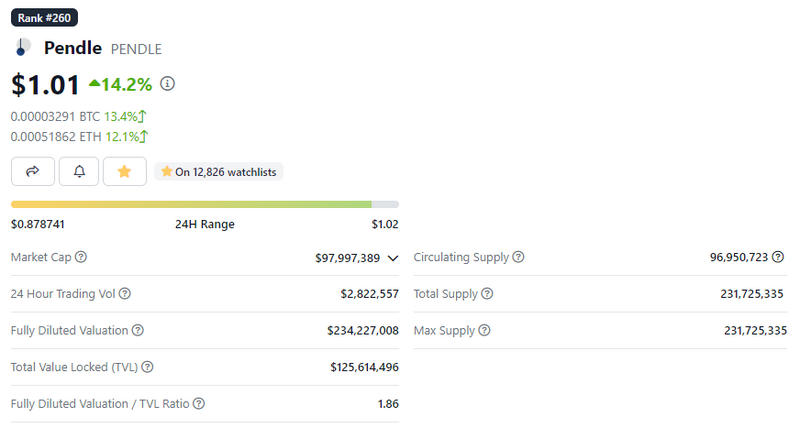

Source: https://www.coingecko.com/en/coins/pendle

Pendle has been one of the most successful protocols in encouraging token holders to escrow their tokens. But why are investors exchanging PENDLE for vePENDLE?

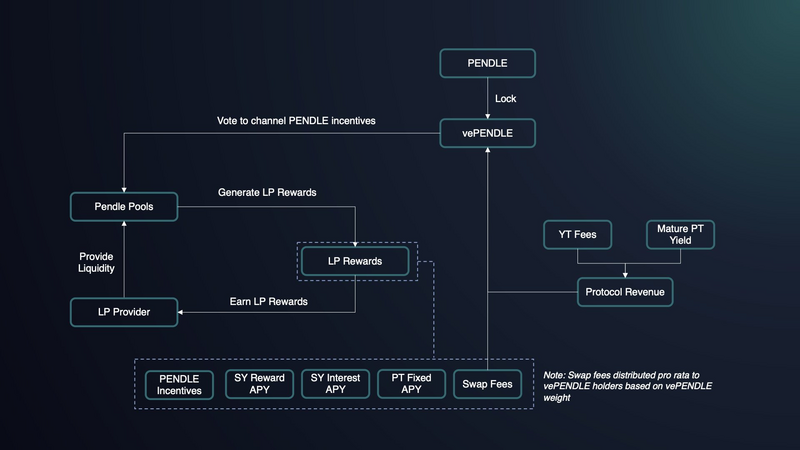

Source: https://docs.pendle.finance/ProtocolMechanics/Mechanisms/vePENDLE

vePENDLE has a decaying 2-year lock-up period. These holders collect 3% of all the yield accrued by yield tokens and can channel incentives on the protocol. Additionally, they receive 80% of the swap fees from the voted pools, and their LP positions on the protocol have their yield boosted by up to 250%.

Readers will notice the similarities with Curve and even the overlap with Solidly. What did PENDLE get right? Incredibly low incentive emissions and a product people want to use, creating a protocol investors want exposure to.

Conclusion: Every veToken Is Different

Locking tokens primarily provides benefits to the protocol. And for this reason, protocols have become increasingly inventive in their methods to convince investors to lock up their tokens willingly.

Although the models and general incentives for locking tokens have become established, the ultimate result of locking the token comes down to each individual token and the benefits provided by the protocol.

The information and example provided in this article are for educational purposes only and should not be taken as investment advice.

Kofi J has been active in DeFi since the 2020 summer explosion and has been rugged more times than he can remember. He hopes to make the decentralized economy a little bit more accessible through his prose. Follow the author on Twitter @k_pangolin

Or check it out in the app stores

Or check it out in the app stores