DeFi has come a long way since the launch of lending protocols such as Compound and Aave. The composable nature of DeFi allows smart contract developers to build on top of these protocols, creating a new class of financial primitives.

Over the last few months, we have seen increased efforts to tokenize future yield generated from Compound and Aave interest-bearing tokens. We see protocols that give users instant access to future yield by tokenizing and separating the principal and interest portions of future yield. We also see protocols that allow users to take out a loan for “free” and have them paid off automatically over time.

Tokenizing future yield may not seem like much work, but it actually involves incredibly complex mechanisms. In this article, we will be going through some of these innovations and the mechanisms involved. The four projects that we will be going through would be:

-

APWine

-

Pendle

-

Element

-

Alchemix

APWine, Pendle, and Element have roughly similar mechanisms and they allow users to split an interest-bearing Aave or Compound token into separate principal and yield tokens. With the tokenization of future yield, users can sell these yield tokens to lock in the interest rate received or buy these yield tokens to speculate on yield without committing a large amount of capital.

Alchemix, on the other hand, works slightly differently and allows users to receive yield in advance on deposited assets in the form of debt, which is then slowly paid down using the yield generated from the deposited assets.

APWine

Since most returns in the DeFi space are highly variable, users may want to lock in the most profitable rate of return. This allows for countless opportunities where users can profit off the interest rate volatility by purchasing ‘yield’ at low APYs and selling them when the yield rates increase. This is where APWine’s future-yield trading platform comes into play.

APWine works by letting users deposit their yield-bearing assets in exchange for separate tokens that represent the principal and yield respectively. Rather than depositing regular assets such as DAI or USDC like most DeFi protocols, users are only allowed to deposit interest-bearing tokens such as aDAI (Aave’s interest-bearing DAI token), yyUSD (Yearn’s yUSD vault tokens), iFARM (Harvest Finance’s interest-bearing FARM token) into the APWine platform. Doing so entitles users to receive two tokens:

-

Interest-bearing tokens, or IBT representing users’ claim on their deposits. For example, depositing 1,000 aDAI tokens will mint IBT representing the claim to these 1,000 aDAI tokens.

-

Future yield tokens, or FYT representing the future yield that will be generated by an asset over a specified period of time (30 days cycle during the beta test). Continuing the above example, the 1,000 aDAI deposited will also mint 1,000 FYT, with each token representing the yield generated by 1 aDAI over a 30 day period.

Let’s assume that Aave’s variable interest rate for DAI is currently 12%. If you want to lock in the current interest rate, you can choose to sell the future yield tokens, perhaps at a discount, to receive a maximum return of $10 upfront.

Regardless of future movements in yield rates, your earnings are already locked in. If it decreases, then you have effectively shorted yield rates. On the other hand, if rates were to increase, the future yield tokens would have given a higher return instead, had you not sold them at the start.

A key concept to note here is that users have to burn FYTs together with the IBTs to unlock the initial deposits. This means that you essentially forfeit the yield generated so far if you choose to exit before the end of the period.

However, users don’t have to exit once the cycle ends since they can roll over to the next cycle by keeping their assets deposited and will receive a new series of FYTs when it starts. IBTs are transferable but only the owner of the tokens will receive new FYT tokens upon each new cycle.

Note that if users choose to deposit in the middle of the cycle, they will have to wait until the cycle ends, before receiving FYT at the start of the next cycle. These tokens can then be traded like any regular ERC-20 token, where users can sell them immediately to receive the locked yield upfront. Otherwise, users can choose to wait and burn the tokens upon the period’s expiration in order to claim their generated yield.

However, the protocol is also subject to the same challenge faced by many other DeFi projects in bootstrapping liquidity. There may also not be sufficient buyers for the yield tokens, which may result in depositors having to hold these tokens without much-added benefits.

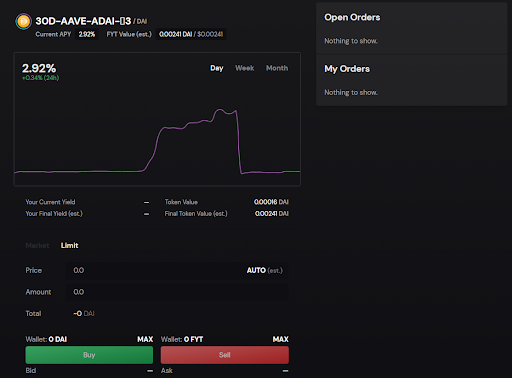

APWine has included an “AUTO” feature that automatically calculates the estimated fair value of the yield tokens at any point in time, making it easier for users to get the best price for their returns. You do not have to be an existing participant of APWine to make use of the exchange.

Recently, APWine has conducted a Liquidity Bootstrapping Pool for APW, the governance token of the protocol. Token holders will receive benefits such as the ability to shape the project’s future through governance decisions.

Additionally, 5% performance fees are collected from the yield generated by the deposited interest-bearing assets. 0.05% trading fees collected from trades conducted on APWine’s own Automated Market Maker (AMM), which will be implemented in the future, will also be redistributed to token holders. Similar to the token design of Curve Finance, APW tokens can be locked for up to 2 years to receive a larger share of voting power and rewards.

The beta version of APWine was launched on 15th February 2021 on the Ethereum mainnet, which featured 3 different markets for future yield as mentioned above. Currently, version 1 of APWine is still in the works and is expected to be released in the coming months.

From a trader’s perspective, APWine introduces a capital-efficient way to speculate on interest rates, without having to lock up huge amounts of capital to gain the same level of exposure. As the FYT approaches maturity, the token’s price should converge to the realized yield generated by the interest-bearing tokens. As such, users can choose to gain exposure by purchasing FYT if they expect interest rates to increase before the period ends, where they can sell it at a higher price before maturity or use it to claim the generated yield.

As opposed to options, which are more of a leveraged bet on highly volatile assets, this is more akin to betting on the productivity of an asset, which serves as a viable proxy especially for stablecoins that are considered fairly nonvolatile.

Pendle

Similar to APWine, Pendle aims to separate capital and yield into two distinct parts, where the latter can be freely traded on Pendle’s own Automatic Market Maker (AMM). Users can deposit their interest-bearing assets onto Pendle to mint future yield tokens, which can then be used to provide liquidity on the AMM, earning swap fees and PENDLE token reward.

Users can also opt to sell their future yield tokens for cash up-front, allowing them to lock in fixed interest rates immediately and thus remove volatility from their expected returns. After selecting their preferred asset and expiry date and depositing their interest-bearing tokens, users will receive two types of tokens:

- Ownership Tokens, or OT, representing ownership of the underlying assets in Pendle for the chosen duration. OT holders can withdraw their assets at any time after the contract expiry date at a 1:1 rate. If OT holders want to withdraw the underlying asset before the contract expires, they would also need an equivalent amount of YT and OT.

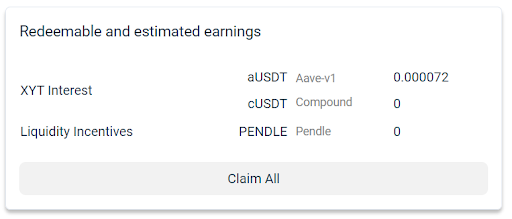

- Yield tokens, or YT, representing the yield generated by the deposited assets for that particular duration. As long as users are in possession of YT, they are entitled to claim the yield anytime which will slowly accrue as time passes. The claimable yield is indicated on the dashboard as shown below.

If holders want to withdraw before the contract expires, they would also need an equivalent amount of YT and OT. For instance, holders would need 1,000 YT and 1,000 OT to withdraw 1,000 units of the deposited asset. There is also a renew function where holders can automatically move deposits forward into the next contract period.

Pendle’s AMM allows users to provide YT and the underlying asset as liquidity to earn 0.35% swap fees and PENDLE token rewards. For example, liquidity providers that choose to provide YT-aUSDT must also prepare an equivalent amount of USDT.

Users may choose between dual asset or single asset staking, where the latter will only require YT tokens. In exchange for providing liquidity, users will receive PendleLP tokens which represent the share of the liquidity pool that can be staked to earn extra rewards.

Since yield is claimable as time passes, it is only natural that the intrinsic value of the YT token will depreciate over time and become valueless as it hits maturity. Therefore, Pendle’s AMM has been designed to mitigate the effect of time decay on liquidity providers, by shifting the constant product curve of the AMM as the contract approaches maturity, as shown below.

In simpler terms, the goal of curve shifting here is to reduce price divergence as expiry approaches, thus limiting larger arbitrage opportunities. If a regular constant product curve is implemented, LPs will stand to suffer heavy impermanent loss as sellers would quickly rush to sell their YT before it goes to zero.

It is important to note that Pendle markets will not have full functionality for the whole duration of a specific YT contract and they actually exist in three states - active, frozen, and expired.

Frozen states are denominated in days and calculated by dividing the contract duration by 20. To illustrate, a 600-day YT contract‘s frozen state will initiate when there is 1/20 days left in the contract duration, or 30 days before expiry. During the frozen state, swapping tokens and providing liquidity will be disabled, while withdrawal of liquidity is enabled as trades that occur during this period are not really meaningful. In the expired state, users will no longer receive accrued interest and LPs can choose to renew their positions to a new expiry date or redeem the underlying assets.

We have mentioned the PENDLE token several times, but what is it actually used for? At launch, it will fully serve as a utility token, while governance functions will be introduced at a later stage once the protocol has seen significant growth. The PENDLE token was recently released via liquidity drop bootstrapping, a new innovative way of funding where single-sided liquidity would be added to a Balancer pool at random times over the course of the token distribution event. The platform itself is currently available on the Kovan testnet, while the mainnet launch is expected to arrive on 17th June.

On the surface, we can already see that APWine and Pendle have many similarities such as adopting a dual-token model as well as the withdrawal mechanisms. However, one main difference is that APWine’s yield token only allows users to claim the realized yield at the end of a period, as compared to Pendle which allows users to claim the generated yield anytime, as long as users hold the token. In this case, we can see that Pendle lets users maintain capital flexibility since they can constantly claim the accrued yield and then withdraw at any time, as opposed to waiting until the end of a period to collect the yield.

As previously discussed, the intrinsic value of APWine’s FYT takes into account the yield generated during the entire period, which leads to a pseudo price floor, taken to be the expected yield generated so far as it approaches the end of the period. There should also be a convergence in price to realized yield upon expiry. In other words, less volatility is to be expected.

On the other hand, the price of Pendle’s YT naturally decreases due to time decay, barring spikes in expected yield. The time decay applies here because rational market participants can claim the yield accrued so far and attempt to sell it back to the market, which would lower the price. This ensures a more accurate price as past yield is assumed to be already claimed. Yet, it should be highlighted that accrued yield will constantly be credited to the holder until ownership of the YT is relinquished. In other words, YT sellers do not have to worry about forfeiting their past yield as it is already accounted for and will be claimable at any time.

Element Finance

Element is another protocol that follows the recurring theme of splitting principal and yield into separate tokens. Unlike APWine and Pendle, you can deposit base assets such as ETH, BTC, or USDC, which will then be used by Element to generate yield on other DeFi platforms. Element’s tokens are called:

-

Principal Tokens, or PT, representing a claim towards the deposited assets on Element at a later date. Upon expiry of the contract’s duration, you can use PT to claim the underlying asset. PT can also be purchased at a discount to gain a fixed yield, which will be discussed in-depth later.

-

Yield Tokens, or YT, represent the yield generated by a unit of the deposited asset for the specified term. These yield tokens accrue value over time and can be sold on Element to lock in your realized interest or purchase them to gain exposure to variable interest rates without locking up large amounts of capital.

Since the deposited asset is essentially locked for the duration, there are heavy incentives for users to sell their PT at a discount, should they require the assets in an emergency. By purchasing the discounted PT, holders can claim the underlying asset in the future. This basically allows users to earn a guaranteed yield on the asset.

For example, let’s say that you purchase 11 ETH Principal Tokens which mature in 1 year at a fixed APY of 10%. This means that you pay 10 ETH for it now, in exchange for receiving 11 ETH at the end of the period. When the term matures, you will be able to use the 11 ETH Principal Tokens and exchange it at a 1:1 ratio for 11 ETH, earning a 10% APY after 1 year, which has been locked in from the start.

In the time that you are holding the PT, you can also use it to provide liquidity to an Automated Market Maker. By using the discounted asset and pairing it with the same underlying asset, it is somewhat similar to single-asset staking, since the PT can be redeemed for the same asset at a later date. This allows you to mitigate impermanent loss and boost your yields, earning you trading fees on top of the existing fixed yield.

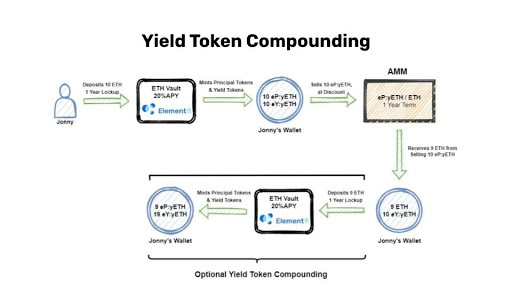

Besides that, another key use case for PT is the ability for you to leverage your assets and compound yield tokens by depositing them into Element to receive PT and YT, selling the PT back into the base asset, and repeating the process again. To illustrate, let’s use the example provided below by the Element team.

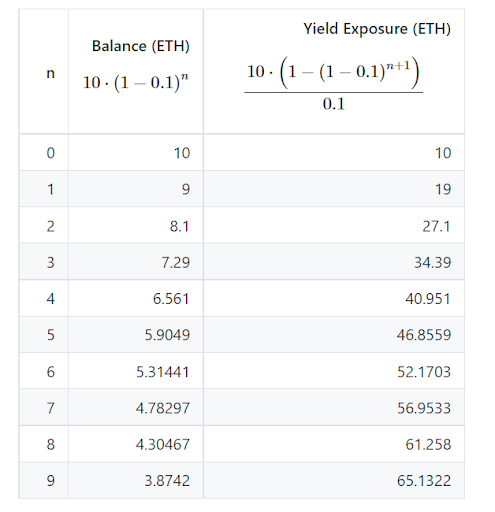

Assuming that you start off with 10 ETH and recursively deposit and sell back your PT to ETH at a 10% discount for a total of 10 times. In the end, you would have slightly less than 4 ETH, yet have over 65 ETH worth of exposure to yield.

This is important because, if you expect interest rates to be consistent or go even higher towards the end of the term, you can now achieve a much higher rate of return instead of just holding to the original amount.

Continuing from the previous example, let’s say that you expect the average APY to increase to 20% at the end of the term, Below is a table that shows the expected return from 10 ETH, with and without leverage.

This strategy essentially amplifies your risk so do be aware that if interest rates were to decrease instead, you will end up with less ETH than you originally started, so do be careful if you do use this strategy. Here, we can already see that the ETH generated from the compounded yield tokens amount to approximately 13 ETH (20% APY from 65 ETH of leveraged YT), which is much more than just receiving 2 ETH worth of yield without leverage. Your returns with leverage will be the remaining 3.9 ETH (from PT) plus the 13 ETH of generated yield (from the 65 ETH leveraged YT). As opposed to earning just a mere 20%, you would now be receiving a 69% interest rate.

This method can be extended into what Element calls De-Collateralize. It has no liquidation risk, requires no collateral, is less expensive, and can be more profitable in the right market. Instead, what is akin to borrowing APY is paid upfront. You get exposure to the yield position and the token of your choice. De-Collateralize is essentially a fixed-term, fixed-rate loan backed by yield positions in the market.

To summarize, Element Finance introduces an added layer of composability for the underlying principal tokens, which brings another dimension of capital efficiency through leverage and yield token compounding. Since the rate of discount at which you acquire the PT and YT from the market is equal to the fixed yield received for the period, it reflects the expectations of the participants on where they think the yield rates are headed.

If you think that rates could be much higher relative to the current discount, you could purely speculate on that using YT. For instance, let’s say that a YT on 1 ETH could generate an average APY of 10% or 0.1 ETH, then the fairly discounted price at the start of the term would be 0.09 ETH. If the discounted price is much lower than that, then you would be strongly incentivized to purchase the YT since you will still be able to claim it for the same amount of ETH.

At the moment, the Element protocol has not announced any form of governance token. However, they are planning their governance system, which will introduce a number of new primitives and seeks to be “modular and flexible”. Element is now available for testing on the Goerli network and is estimated to be launched on Ethereum mainnet by 30th June 2021.

Alchemix

Alchemix is a synthetic asset platform that gives users access to future yield in the present. But what does that mean exactly?

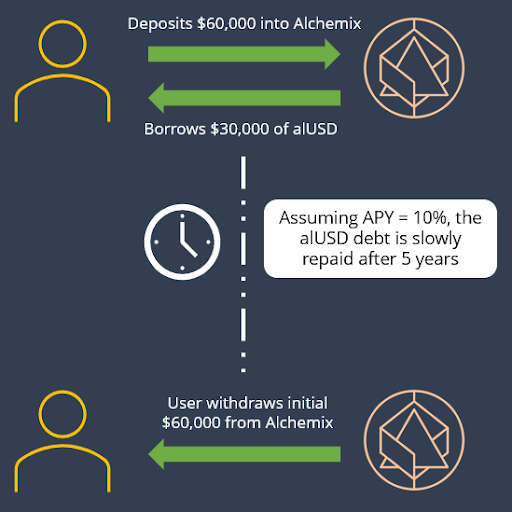

Picture a scenario where you would like to buy a $30,000 car and you have $60,000 in investment assets. With Alchemix, you have the option to buy the car today without having to lose your hard-earned savings.

You can deposit $60,000 worth of assets such as DAI or ETH into Alchemix and withdraw 30,000 alUSD or alETH - both of these are synthetic assets created by Alchemix. You may then exchange alUSD or alETH into other cryptocurrencies such as USDC or fiat currency to purchase the car.

Interest generated on that deposit will be used to slowly repay your loan. After a few years, the loan is completely repaid and you can reclaim your collateral without having to pay back any alUSD. You get back your $60,000 and you now have a car that is virtually free!

On top of that, the debt is totally interest-free and you do not have to worry about liquidation. We will dive into the details on several components of Alchemix that make this work: Vault, Transmuter, and the Alchemix DAO.

As shown by the picture above, with 10% APY, the debt will be totally repaid in five years!

Vaults

Firstly, vaults are the heart of Alchemix and are key to promoting capital efficiency. For now users can deposit DAI into the vault to mint alUSD. The alUSD can then be used to invest or yield farm. This allows users to make the most out of their capital by having the access to future yield today, without having to lose their initial capital.

The maximum amount of alUSD that can be minted is 50% of the deposited collateral, effectively enforcing a 200% minimum collateral-to-loan ratio. Note that there is also a global limit to how much alUSD can be minted for each asset, which serves to mitigate risk for a particular asset. The current global limit for DAI is $125 million.

At the moment, the alUSD vault and their recently launched alETH vault is available for use. At launch, the alETH vault will have different parameters compared to the DAI vault. For example, it will have a higher collateralization ratio at 400%, meaning that you need to deposit at least 4 ETH to borrow 1 alETH. The debt ceiling will also be set at 2,000 alETH.

The DAI deposits are then invested with the yDAI vault by Yearn Finance. Earnings are then harvested, with 10% of the yield collected going to the protocol. The remainder 90% is sent to the transmuter, which is used to pay down the global debt in the Alchemix ecosystem, thus reducing all debts incurred by alUSD borrowers.

As debt is gradually paid down, users can withdraw their initial capital over time. Global debt can be determined by deducting the amount of mintable alUSD from the debt ceiling.

If you are in a rush, you can also choose to repay your debt completely to unlock your funds straight away. The alUSD debt can be paid in either alUSD or DAI since they are both treated as equal for repayment and liquidation purposes. In the worst-case scenario, you can instead choose to liquidate a part of your DAI collateral to repay your loan, but you will not suffer automated liquidation.

For facts and figures on deposits and circulating supply of alUSD, you can refer to https://dyor.fi/alcx/. It even has a handy slider for you to figure out how long it takes for your debt to be repaid!

Optionally, users can choose not to borrow and just deposit their funds to earn yield in the form of an increased borrowing limit. This lets you borrow alUSD without taking on additional debt. In the event that there is no mintable alUSD left, you may still choose to deposit and accrue your increasing borrowing capabilities. In other words, at 10% APY, your 1,000 DAI will allow you to borrow 100 alUSD for free after 1 year.

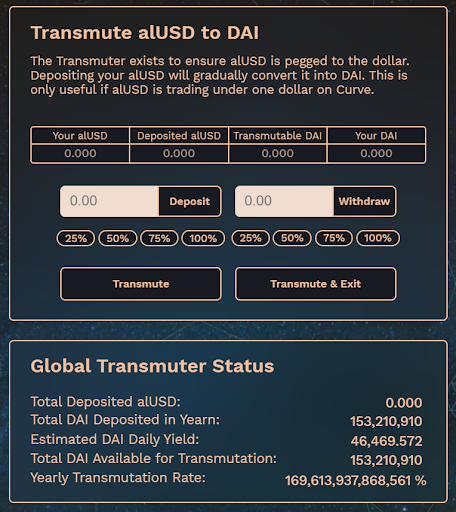

Transmuter

Since alUSD is a synthetic stablecoin, there is a chance that it may be off-peg, allowing users to benefit by purchasing cheaper alUSD to repay their debt. This doubles as a method to restore the peg as more users push up the price by buying more alUSD. Yet, the primary pegging mechanism lies in the transmuter.

The transmuter works to guarantee that a 1:1 redemption of alUSD to DAI is always available to participants. Users can stake alUSD into the transmuter which will allow them to slowly claim a share of the DAI which is flowed into the transmuter after harvesting. DAI withdrawals from the transmuter will cause an equal amount of alUSD to be burnt.

It should be noted that positions can be overfilled, meaning that you can earn more DAI relative to your staked amount of alUSD. In that case, another user can claim on your behalf, which will convert the surplus amount of their staked alUSD immediately into DAI, without having to wait for it to be transmuted. In other words, assuming that you deposit 1000 alUSD into the transmuter but it has been converted over time into 1050 DAI, more than your original stake, then the extra 50 DAI is available for others to claim and convert their own alUSD positions.

If the original owner is the claimant, then the surplus is instead distributed to all users. Here, we can see that debt repayment and claims on yield represent strong use-cases for the alUSD token to maintain its peg. This is further reinforced by the introduction of staking incentives for alUSD on Curve, which offers 30% APY as of the time of writing as well as future dApps that will rely heavily on the stablecoin.

Alchemix DAO

The platform is governed by the Alchemix Dao, made up of ALCX token holders, who are granted voting rights and usage of the treasury. The 10% fees portioned from the generated yield are sent to the Alchemix DAO treasury, and token holders will have the opportunity to earn their share of the platform’s revenues once Alchemix V2 is live.

Currently, ALCX holders can earn up to 140% APR worth of ALCX tokens via single asset staking. The lifespan of this single-asset staking pool is subject to the community’s decision.

Final Thoughts

To conclude, having the ability to tokenize your future yield is an extremely new yet important addition to the DeFi space, where returns are usually anything but fixed. Although interest rate products do exist in traditional finance, there is nothing quite like a product where you can choose to split up your principal and interest, as well as realize your future yield in the present, all done through a permissionless and transparent manner.

The untapped potential here is huge, as interest rate products made up 80% of the outstanding notional value of OTC derivatives, or approximately $467 trillion dollars, towards the end of 2020.

Although these figures are still far from reality for any DeFi protocols at the moment, it is not difficult to imagine DeFi protocols capturing even a small fraction of that amount with such a practical use-case for tokenized yield. With so many new protocols to try and discover, choosing how and where to allocate your capital can become a headache in the pursuit of the highest returns.

By having your yield separated from the underlying principal, users can free up more capital to chase other endeavors, while maintaining exposure to a particular protocol of their liking.

Although these tokenized yield protocols look similar on the surface, they each have their own major differences that will appeal to specific users. Alchemix uses your future yield to pay back a zero-interest loan which you can take immediately, essentially bringing the future yield to the present. If you have the time, it could be a viable choice to deposit and borrow alUSD to experiment with other projects.

On the other hand, protocols like APWine and Pendle, allow you to trade your future yield in order to secure a fixed rate or to allow for greater yield exposure with minimal capital. Element Finance adds additional utility for your principal by allowing you to continuously sell your locked principal to recursively deposit into the protocol, thereby creating a form of leveraged yield farming through compounding yield tokens.

The differentiator here is what dictates the effective fixed rate for each protocol, so to speak. In Alchemix, since the yields on your deposited DAI are variable, we can say that your effective rate is determined by time. Let’s say that you borrow 50% of your collateral in alUSD and the debt is completely repaid by the yield from your deposited DAI in 1 year’s time. Then we can say that you have earned a 50% APY on your DAI. The longer the time it takes to repay your loan, the lower your effective yield rate will be.

This is different from the other platforms, where the price at which you sell your yield tokens will determine the total fixed amount received. However, for Element, the earned yield on the principal tokens is determined by the discount rate at which you purchased them.

Currently, only Alchemix is live while the other three are still in the testing phase. Alchemix has amassed an impressive adoption rate, with Total Value Locked (TVL) reaching $1.23 billion, based on DeFi Llama, ranking it at number 26 among all DeFi protocols, albeit with liquidity mining incentives.

Although there is a huge appetite for novel financial products, it remains to be seen whether the dual-token model (principal and yield tokens) adopted by APWine, Pendle, and Element will gain significant adoption. For further reading on fixed yields, you can also refer to our other article on Fixed Interest Rate Protocols (FIRPs).

As with all other DeFi protocols, the real challenge is to capture the available liquidity in the space, either through sustainable incentives or superior products. Although power users would be more interested in these new types of primitives, it is not impossible to envision a future where retail users can be just as excited and learn to use these protocols as part of their investment strategies.

Or check it out in the app stores

Or check it out in the app stores